Investing Theory and Pilbara

I have been reading the book “The Most Important Thing Illuminated: Uncommon Sense for the Thoughtful Investor” written by the billionaire fund manager Howard Marks lately. It’s a very good book that covers some very important mind set tools, that is useful for any stock picker in my opinion… Anyway, I thought it would be fun (and hopefully helpful) to cover some concepts and how it relates to Novo Resources and the Pilbara Juniors (in my opinion).

Mark’s definition of an efficient market situation (Where no alpha return opportunity would exist):

investing5

Those comments are about asset classes but I think it’s relevant to use on a case by case basis as well. So lets apply this to Novo and the Pilbarians and have some discussion whether they could be considered to be efficiently priced or if there is opportunity for undervaluation (or overvaluation)…

- The asset class is widely known and has a broad following.

I would argue that this is a NO. My take is that it’s not really well known (other than perhaps by name), and that the majority of sell side analysts and newsletter writers have no incentives to follow the company, since Novo is all cashed up and it’s such an unconventional case that requires a lot of time and energy to summarize for clients and what not. Furthermore, during bear market sentiment when capital is scarce, the last thing most promoters would want is that capital gets diverted anywhere but into their respective companies of interest, and the bigger the potential, the more capacity for capital soaking there is.

I have listened/watched a few podcasts/videos where some of the more famous newsletter writers have been asked to discuss primarily Novo. It’s immediately obvious that they have no clue what Pilbara is about and only focus on the challenges of “nuggety gold” and that Novo supposedly has “no resources”. In regards to the former claim, they constantly leave out the Hardey Formation at Beaton’s Creek and make it sound like they have no clue about Novo’s other prospects and/or that the Karratha Mt Roe is different from the Nullagine Hardey Formation conglomerates. On the latter claim, it again shows that they intentionally disregard Beaton’s Creek or again, have no clue that it’s a stand alone project with different geologly. Even Brent Cook makes it sound like he is still stuck in 2017, and has not commented on either Egina or Beaton’s Creek (Hardey Formation) over the last 12 months when asked about Novo. Basically, they give the impression that Novo and Pilbara is a “one trick pony” that would rise and fall with one project (Comet Well/Purdy’s Reward), which in itself is just a fraction of the Fortescue Basin.

Furthermore, most commentators give the impression that they treat the Pilbara prospects as a conventional case, with conventional upside (especially when they stick to just comparing resources to resources), even though it should be rather obvious that a rational person would want to evaluate and value future upside scenarios and thus growth potential. There is a reason why the early discoverers of the Wits reefs probably ended up being rather bitter that they sold their rights based on the currently known prospects and conventional thinking etc. No one had seen such a vast gold bearing system before so there was no precedent to lean back on and visualize what else might be hidden down dip. That is why it really boggles my mind that few “outsiders” acknowledge the sheer size potential since we already have a precedent in terms of the similar aged Witwatersrand gold fields.

I would argue that the following went down with the share price, and very few ever bothered to check up and realize that Novo and Pilbara has transformed a couple of times over the last 12 months including; 1) Potentially basin wide lag gravels sourced from pre-existing conglomerates and lode gold, 2) The fact that there is no theoretical gold operation more suited for “3D concentrated” gold system in the form of nuggets and the proximal secondary precipitation gold halo, 3) The nugget effect at Beaton’s Creek Hardey Formation system leading to an under-representation of grade up to potentially 50% (i.e. might be up to twice as rich), and 4) The sheer amount of conglomerate gold and/or eroded nugget patches that has been discovered by pretty much every junior who owns some parts of the relevant rocks.

In my opinion, there are still plenty of long time Novo holders who does not fully appreciate the diversity of targets and/or the scale of the targets in my opinion… Given that, does one expect any newcomer to read a presentation and be able to get a clear view of what prize the Pilbarians are hunting? No way.

- The asset class is widely is socially acceptable, not controversial or taboo

I would argue that this is also a NO. First of all, Novo and the Pilbarians are in the gold business, which has been unloved and sometimes even ridiculed for many years no (“Gold bug” anyone?). Second of all, Pilbara is probably the most or at least one of the most controversial plays in the sector. The mere mention of a “Wits analogue” gets you laughed out of the room. If that’s not enough, trolls were early to start throwing “Bre-X” around and that there was no chance in hell that another “super basin” could have been found. It mattered little that Pilbara as a whole is very under explored and the fact that at least the Mt Roe conglomerates hosts very nuggety gold, that would explain the lack of (limited) drilling success, was not taken into account. The consensus seems to be that there is simply no way that any super district scale gold systems could be present that would not have been discovered by now. In my opinion, Quionton said it best when he commented that everyone had been looking for a Wits copy (meaning well sorted quartz pebble conglomerate), and the concept of a high energy, poorly to semi-poorly sorted, bouldary mafic conglomerate was so out of the box that no one had previously been able to piece it together.

Furthermore, there are a bunch of newsletter writers and what not who love to bash primarily Novo, probably for click bait purposes and in efforts to divert money from a large(r) cap company into their own micro cap lottery ticket pumps. This of course might lead to newcomers simply not bothering to even take a look at Novo and Pilbara, which has transformed many times over just in the latest 12 months. Lastly, I would say that the “oh, they got some alluvial gold” and “oh, look it’s a new version of the show Yukon Gold Rush” comments with an implied smugness are telling in terms of the consensus being that all alluvial deposits are the same, and that it is no different than some alluvial creek bed in Canada for example (and no further due diligence is warranted). Not only does that look to be completely untrue, but there are and have been big alluvial operations all over the world.

- The merits of the class are clear and comprehensible, at least on the surface, and

- information about the class and its components is distributed widely and evenly.

I would argue this is a big and fat NO. First of all, as discussed earlier, Pilbara is anything but “clear and comprehensible”. For example, some view Novo as a “one trick pony” in regards to the Comet Well/Purdy’s Reward project. Not only is this just ONE prospect out of multiple prospects that have been mapped, but it’s also just one of many targets. To get a complete picture of Pilbara, one would have to follow every single company that are proving up different parts of rock formations that transcends any junior’s claims. Not only that, but the story continuously changes as we have seen over the last 12 months. Most recently we learned that the ore sorting results for the mafic Mt Roe conglomerates at Comet Well were out of this world but also that at least parts of the Hardey Formation seems to be gold bearing in western Pilbara as well. In terms of the former, one has to keep in mind that ore sorting seems to be a technology that few have any real experience with. I can only speak for myself, but ore sorting was not something I had even considered before Novo came along. Outside Moriarty and Barron, I don’t think I have seen a single newsletter writer or pundit talk about it and the Novo share price retraced its gains in a matter of days (i.e. the market’s judgement is that it has no impact at all on the fundamentals). It was the same story when Egina was announced by a clearly excited Quinton Hennigh. The share price barely budged, which implies that the potential discovery of a district scale lag gravel horizon (which is near surface and appears to be drillable due to the fine gold component) supposedly meant nothing for Novo’s long term value proposition, which is a ridiculous notion in my opinion. The area has been mined for a 100 years and even up to this day. I am happy to bet against such consensus and hopefully reap the rewards of such market inefficiency in the future.

The heart of the matter, as I see it, is the fact that Novo are going full steam ahead with Egina (bulk sampling and plant design), Beaton’s Creek (bulk sampling, updated Technical report and nearing a deadline for MOu with Sumitomo) and are preparing Comet Well for a mineralization report… Meanwhile, the market did not discount/care about Egina, the preliminary samples that leads Novo to believe Beaton’s Creek is perhaps up to twice as rich, the ore sorting results blowing out expectations nor a “small” detail such as New Fronteer Explorationa and Kairos finding signs of the Hardey Formation being gold bearing in the west too (The same rock unit that CRA intercepted 10.67 g/t gold over 0.5m in a hole located 50km south of Comet Well).

To sum up the consensus:

- Egina style lag gravels has NO potential value what so ever.

- The preliminary big hike in grades at Beaton’s Creek offers NO potential value what so ever.

- Probably the best ore sorting results for any gold company in the world offers NO potential value what so ever.

- Finding gold believed to be sourced from the Hardey Formation tens of kilometers apart offers NO potential value what so ever.

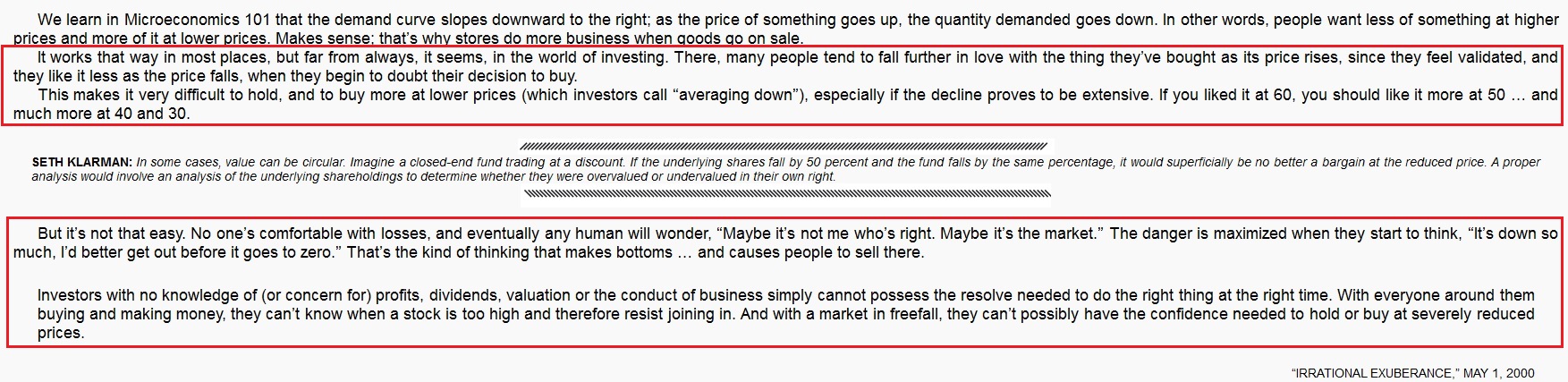

… One might argue that since the market did not really discount much if any of the above developments, that would imply that an investor could bet on any chance of success without any taking any theoretical downside… And such extremes would never happen in an efficient market, because there is no such thing as absolutes in terms of the future. Would you consider the SP movements of Novo and the Pilbarians to reflect an efficient market, with no hopes of beating it…? Food for thought.

Any time new information surfaces, one has the opportunity to bet against the consensus; Sell if one believes the consensus (the market) is too optimistic in terms of the new information’s impact on Expected Value, or buy if one believes that the market is too pessimistic in terms of the new information’s impact on Expected Value.

The only way the share price action over the last months make sense is if one looks at it from a personal and psychological point of view in my opinion. We all know we have been in a beark market and we all know that we have been smack in the middle of tax loss selling season. Negative sentiment and tax planning efforts have seemingly resulted in “sell whatever news” actions by the market. Thus, the impact on Expected Value (or instrinsic value if you will) has been overshadowed and neutralized by rational- (tax planning) and irrational (sentiment) selling because there is no way in hell that Egina, Beaton’s Creek, ore sorting OR the Hardey discoveries would not budge the long term prospects for Novo (or the Pilbarians for that matter).

… I for one am betting against the market/consensus on all points, since I don’t believe in absolutes, but rather discounted possibilities. I am obviously not alone in this given the fact that Novo are already looking at plants for Egina, Beaton’s Creek has 12 people stationed there and Sumitomo has NOT withdrawn from the MOU, Novo are getting ready to file a mineralization report for Comet Well and the Hardey Formation covers huge areas in West Pilbara. Last month @Lemand spoke to Keith Barron who is convinced the conglomerates will be “a licence to print money” and that Beaton’s Creek will indeed become a mine.

Some additional snippets from the book to wrap things up (I might do more articles about all this in the future):

Investing. Source: “The Most Important Thing Illuminated”

… Who is the fish? The market that does not discount, or someone that does discounts, if even in a small degree?

Investing. Source: “The Most Important Thing Illuminated”

… If you believe the market is always 100% efficient, then you have lost the battle for Alpha before it even started.

Investing. Source: “The Most Important Thing Illuminated”

… There are never any guarantees that the market can’t get much more irrational, both to the upside and the downside than what one would expect.

Investing. Source: “The Most Important Thing Illuminated”.

… If it was easy, everyone would be a millionaire. Being a contrarian due to holding firm in the face of a bear market is going against human psychology, and is thus designed to be inherently hard. Everyone should make up their own mind in terms of what Expected Value should be reflected in Novo and the Pilbarians and not change it due to share price gyrations at sentiment extremes. If it’s lower than the Enterprise Value, then one should be out, but if it’s higher, one should just sit tight or add more. I know where I stand and I put no value in the notion that the market is anywhere close to being able to somewhat rationally value Pilbara, because the outcome scenarios for each project and system have the widest range I have even seen in this business. Were insiders at Kirkland Lake fools for buying more Novo at $5 or is the market totally clueless for not discounting anything over the last couple of months…? Food for thought.

If anyone is interested in getting a copy of the book that has been discussed, it can be found HERE on Amazon.com (Note: This is an affiliate link).

Best regards,

The Hedgeless Horseman

Follow me on twitter: https://twitter.com/Comm_Invest

Follow me on CEO.ca: https://ceo.ca/@hhorseman

Don’t forget to sign up for my Newsletter (top right on front page) in order to get notification when a new post is up!

If you want to learn more about Novo Resources and the Pilbara Gold Rush you can purchase all my premium content HERE.

If you find my work valuable and want to help me keep publishing most of my research for free then please consider making a donation, no matter how small.

(There is also a donation button in the top right of the home page)