Two Nickel/PGM/Copper+ Plays: Magna Mining & Stillwater Critical Minerals

In this article I will briefly discuss a few Nickel/Copper/PGM Juniors that I think are some of the better ones out there. Consider me biased. I own shares of both and they are banner sponsors.

Companies mentioned in this article:

- Magna Mining

- Stillwater Critical Minerals

Magna Mining – The Empire Builder

Magna Mining is perhaps the longest standing core position in every “HODL-folio” I manage. It has been a holding for years and I think Magna today has more growth potential than ever before. The runway for growth combined with an exceptional management team makes Magna maybe the most obvious “just sit and wait” cases that at least I am aware of. With exceptional management the surprised tend to happen to the upside like Magna picking up advanced projects for fire sale prices in the last few years. Magna’s team happens to be world experts at unlocking exactly the types of projects which have been picked up so one cannot ask for lower execution risk.

The only way to capture the Alpha from an exceptional team is with time. More time means more cumulative upside surprise potential. Length of time held should thus correlate with returns received all else equal. And with the amount of deposits and targets Magna has to work with today there is certainly a lot of real and potential value to unlock over the coming years:

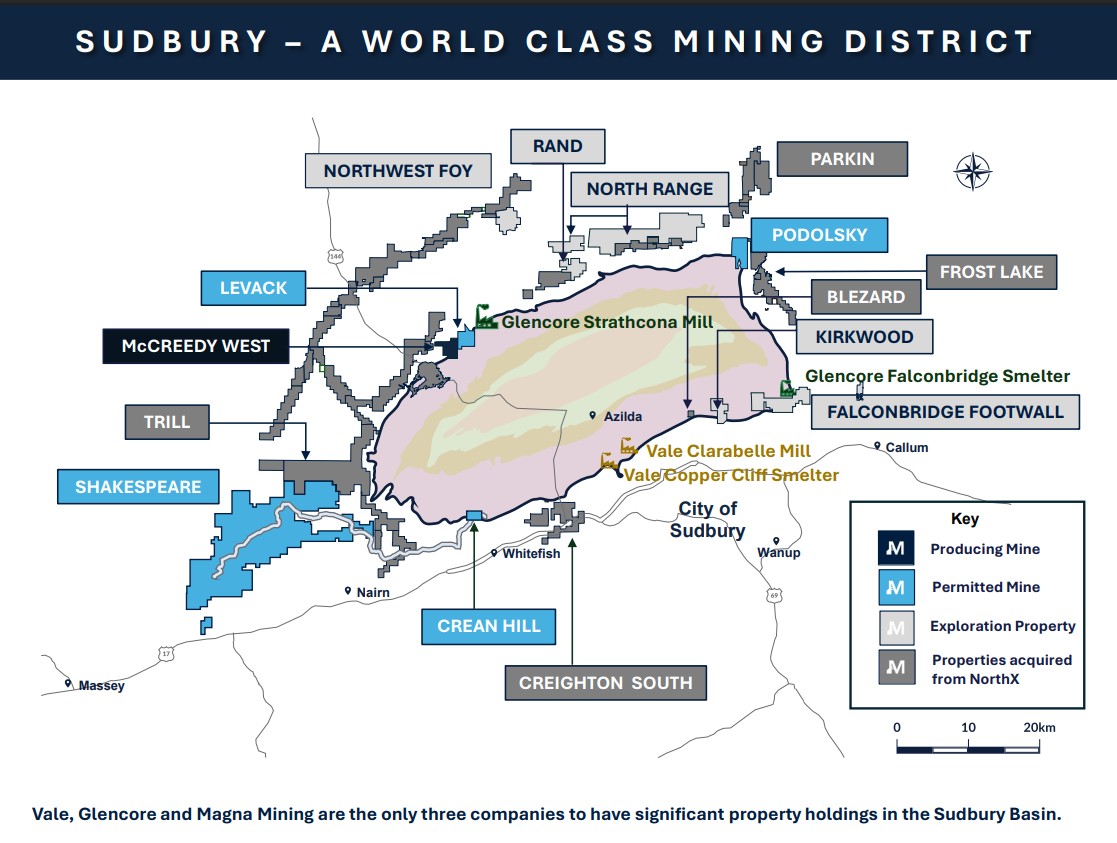

… It is almost unique for a junior to have one producing mine, four permitted mines, and a whole lot of grassroot ground in a Tier 1 jurisdiction. Let alone one of the most legendary mining camps in history. And to top it all off said junior also has maybe the only team around that has literally done this before. And by literally I mean they literally worked on some of these EXACT deposits/mines before. I have even told management a few times that this story is so good it is boring. All I have had to do, and plan on keep doing, is to be along for the ride… For maybe years to come. It’s not a high risk story and there is no point in second guessing a single decision this type of management does. Especially since they have incredible skin in the game and have a lot more to lose than you or I.

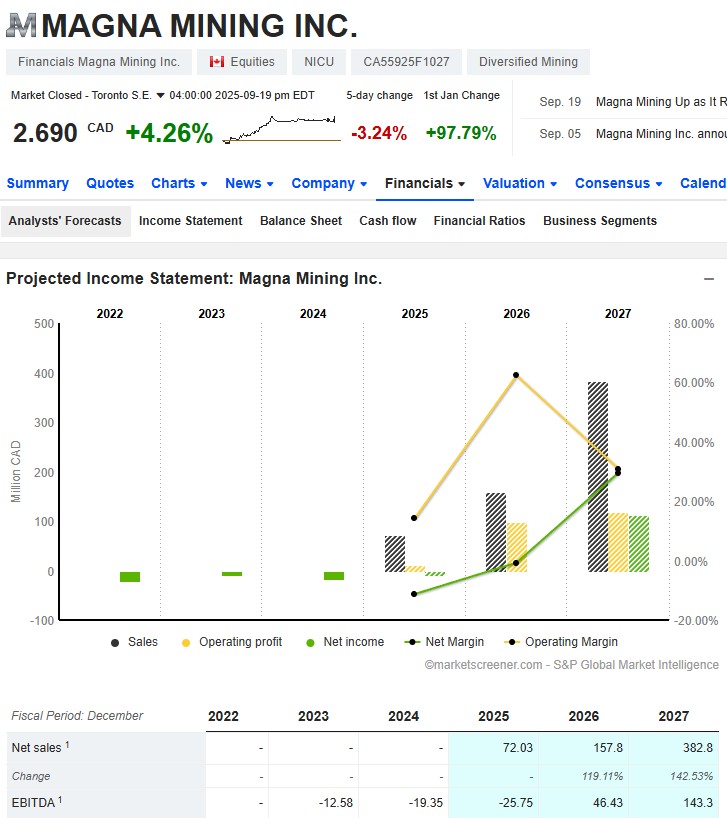

Below is a screenshot of the analyst consensus for Magna up until 2027 and I think that this company could still be on a growth trajectory 10 years from now assuming it has not been acquired.

Magna’s MCAP is currently C$571 M which probably makes quite a few people think there can’t be that much upside left. But consider a scenario within five years where Magna has 4-5 mines up and running at the same time while maybe most metals have gone up in price as well. I think that is a credible scenario given the management team and if that happens it will probably be trading at multiples of today’s MCAP. Add in exploration success, and possibly further accretive M&A as upside surprises on the way, and it becomes quite easy to see how much upside potential is left. In short I think Magna is around as cheap as it was at a 75% lower price and with 75% less assets. This is the simple reasoning why Magna is still a staple in all HODL-folios.

Stillwater Critical Minerals – The District Play

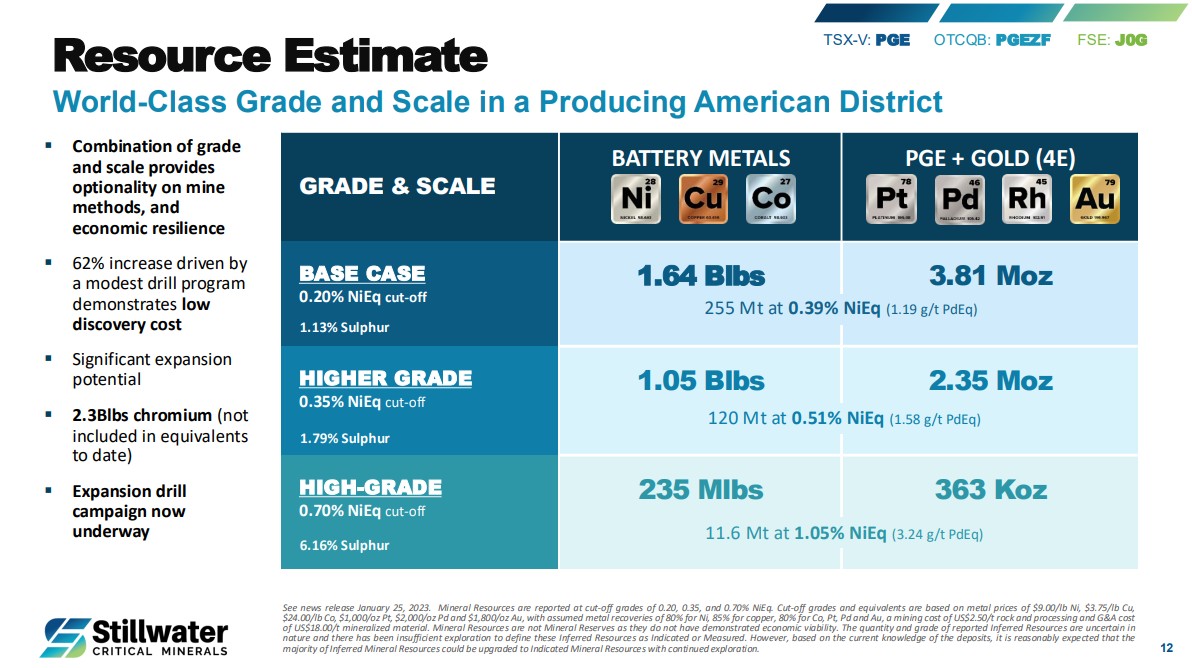

The upside for Stillwater is pretty easy to grasp as this company’s main backer is the C$70 B company known as Glencore. A company the size of Glencore obviously needs billion dollar projects to move the needle and at the time of writing Stillwater has a MCAP of C$107 M. Now why would a C$70 B company care about this C$107 M junior? Well because Stillwater is already sitting on billions of pounds of Ni/Cu/Co and millions of ounces of precious metals for starters:

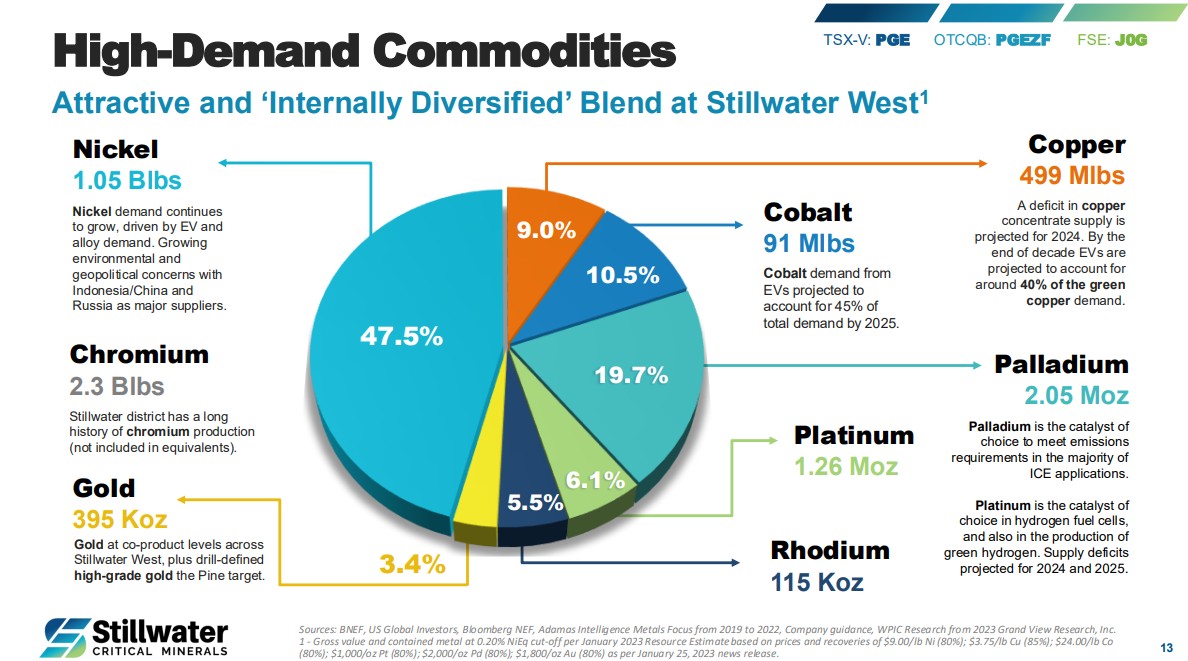

Their deposit hosts a swath of metals/minerals that are considers critical to the US and the deposit happens to be located in the US to boot:

Given the current tailwinds for such metals from a political/geopolitical perspective in the US I would not be surprised to wake up one day and see government (free) money get thrown at Stillwater. This deposit alone would kill a lot of critical/strategic mineral birds with one stone. The fact the $35 T US economy only has a single primary nickel mine highlights how fragile the situation is.

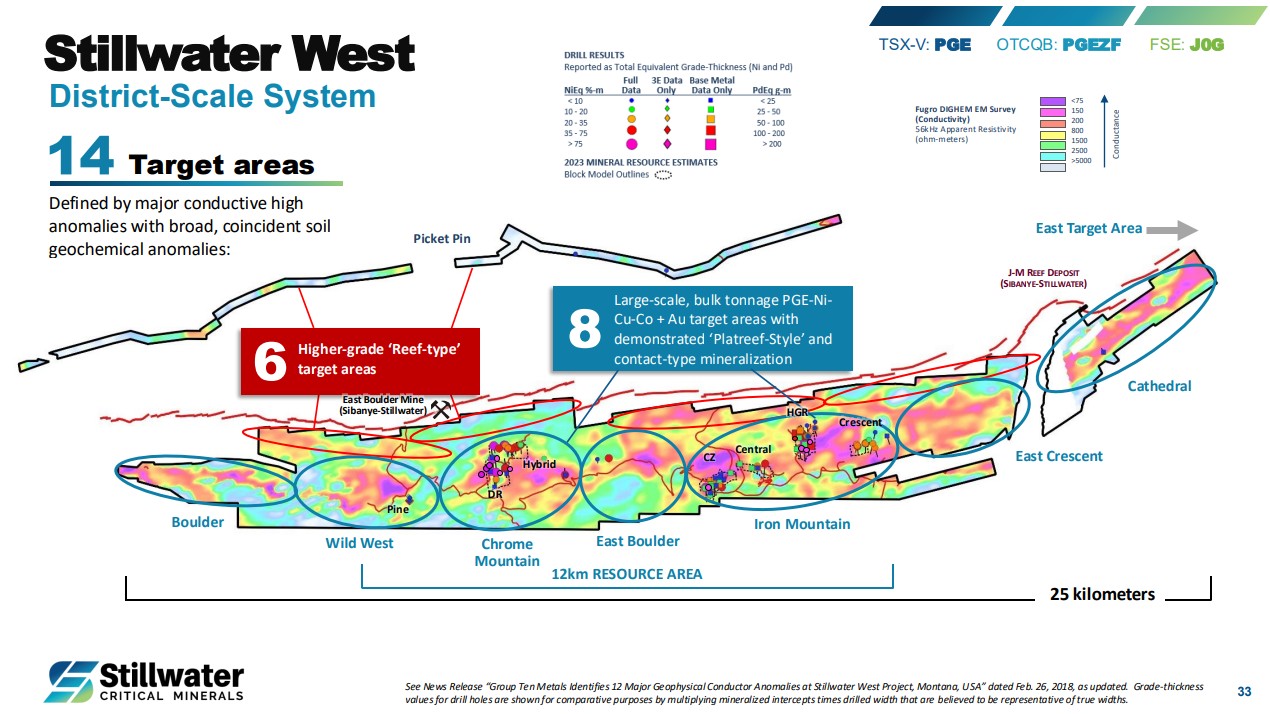

The longer term blue sky scenario for the project, and thus the company, is that there is absolute massive exploration potential here:

To summarize Stillwater is thankfully a simple case (Good Risk/Reward cases tend to be); They already have a deposit, a C$70 B backer as third party validation, geopolitical/political tailwinds, and remarkable exploration potential.

Note: I own shares of Magna Mining and Stillwater Critical Minerals are passive banner sponsor so consider me highly biased. Always do your own due diligence and form your own opinions. Investing in junior miners can be very risky and never invest money you cannot afford to lose. This is not investing advice. I cannot guarantee the accuracy of the information in this article. I share neither your losses or your gains. Assume I might buy or sell shares at any time. I will not be able to hold anyone’s hands 24/7.

Best regards,

The Hedgeless Horseman