THH – Headwater Gold (HWG): #12+ Projects, Three Major Miners Involved, C$32M in EV

This article will outline my investment case for Headwater Gold. I will also discuss some of the positives of the prospect generator model. As I own shares, family members own shares, and the company being a new (passive) banner sponsor you must consider me biased. I cannot guarantee the accuracy of the information in this article so do your own due diligence. There will be personal opinions, personal guesstimates, and forward looking statements. I have not been paid by anyone to write this article but again, consider me biased for the former reasons. For your own sake assume I may buy or sell share at any time and never invest in anything just because someone else is. Consider this a “High Risk/High Reward” case where success is absolutely not guaranteed. There are no guaranteed wins, only Risk/Reward. This is not investing advice or a buy recommendation!

Headwater Gold (HWG.CN) in short

- Insiders/management owns 30% of the company so they have huge incentive to make good decisions for shareholders since no one has more to lose or gain

- Massive Third Party Validation

- Newmont Mining is a 7.1% shareholder and is currently earning into the Flagship Spring Peak Project as well as the Lodestar Project

- Centerra Gold is a 9.9% shareholder and has selected to earn into the Crane Creek project.

- OceanaGold has selected three projects to earn into.

- Rick Rule and Jeff Phillips own 4.1%

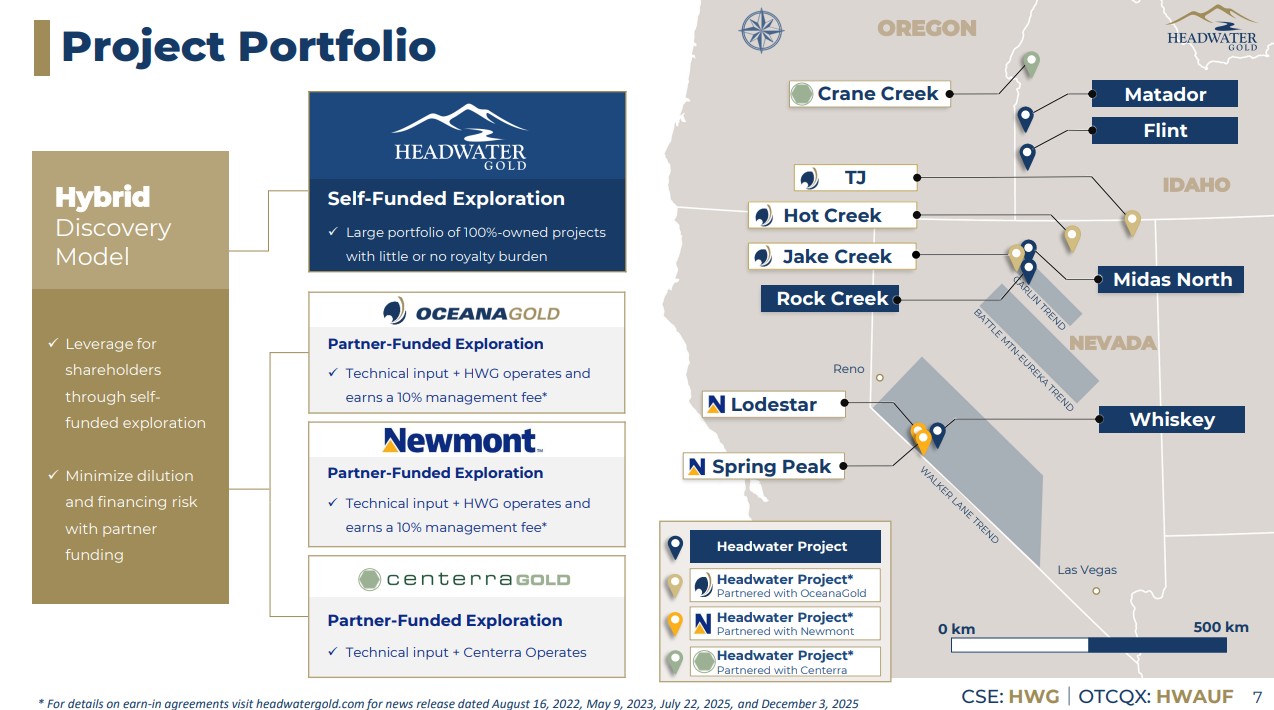

- The company has #12 Low Sulphidation Epithermal projects: all located in the the Western US

- Flagship “Spring Peak” project is in Nevada: Top tier jurisdiction (Permitting, rule of law & jurisdictional Premium)

- MCAP (Basic): C$39 M at $0.44/share

- Cash: C$7 M + 10% ongoing Management Fee revenues

- Enterprise Value: C$32 M

- … That translates to a per project valuation of $32/12 = C$2.7 M per project at face value

- … And the company will likely keep generating more projects to add to that.

“If you’re interested in the high leverage possibilities of a technically driven junior explorer I don’t think there is any better value out there than Headwater.”

If these 12 projects were in their own public vehicles there is no chance that they would have an average Enterprise Value of C$2.7 M. You can only really get such an extreme discount on high quality projects if they are in the same vehicle where Mr Market cannot consciously value 12 projects at the same time. When you have a setup like this it is akin to getting multiple junior explorers but only really paying for one. On that note I amused myself by asking ChatGPT to estimate the risk-adjusted value of Headwater’s current portfolio and this was the result:

… I don’t think these AI generated guesstimates are crazy at all and the resulting combined risk-adjusted value is C$124.5 M compared to the current Enterprise Value of C$32 M. One would have to make some extremely pessimistic chance of success odds in order to fit this portfolio into a C$32 M combined risk-adjusted portfolio value. Make no mistake, Newmont only cares about the potential for a multi-billion dollar district and OceanaGold and Centerra probably wants to see the potential for at least a >$1 B to care about any exploration project. Viewed from that lens these numbers do not seem to be pricing in an overly optimistic chance of significant success for any project. If even a pretty conservative numbers exercise leaves a case looking cheap then that is a very good sign it might really be providing an attractive Risk/Reward proposition.

(Overview of projects created by me)

Note that there is more value in Headwater than is captured in the presentation in the form of Management Alpha. What I mean by this is that the company is actively working on generating new projects and potentially new earn in deals. These can be considered “invisible” catalysts since they are not obvious but implied. For example, lets say the company is able to stake one new project, every 12 months rolling, and is also able to get an earn in deal on it with a major company. If one just puts a C$8 M risk-adjusted value on that new project then that is an extra, continuous ~25% risk-adjusted value “yield” relative to the current Enterprise Value which is highly significant. This kind of Alpha generation is great because it increases the upside potential while it also decreases the risk. If one considers Headwater to have 12 lives (projects) right now it might also be (re)generating an extra life per year into the foreseeable future so it ought to be unusually hard to “kill” the story while it also enjoys an unusual amount of avenues that can lead to upside surprises.

I dare say Headwater Gold is one of the most beautiful cases from an investment theory perspective. This might be quite literally one of the best, if not the best, overall Risk/Reward I have seen in an early stage explorer since I started investing in this space.

Expected Catalysts in 2026

- Jake Creek drilling (STARTED) — program updates, and assay results from the planned ~3,500 m program.

- TJ geophysics results — CSAMT and gravity survey results, followed by refined targets and possible drill planning.

- Next phase of drilling at TJ – follow-up after the new geophysics results

- Lodestar IP survey results — follow-up geophysics over the Meridian Zone, with potential next-phase drilling.

- Spring Peak permitting — FAST-41 / Burnt Rock Plan of Operations milestones or approval, enabling a larger drill program.

- Crane Creek Phase 1 drilling — Centerra-funded first drill program, including drill-start news and assays.

- Jupiter first systematic exploration — mapping, sampling, geophysics, and potential initial drill-target definition.

- Additional drill-program announcements — possible new drilling across partnered or 100%-owned projects.

- Potential new acquisitions — new project staking or acquisition news.

Recent News

Headwater Gold Inc. is pleased to announce that Mr. Joshua Carron has joined the Company in the role of Vice President, Exploration to be based in Reno, Nevada.

- Appointment of Vice President, Exploration: Joshua Carron has joined Headwater as Vice President, Exploration, bringing over 20 years of gold-focused experience spanning exploration, project development, mine geology and operations;

- Direct Experience at Nevada’s Most Recent Major Discovery: Mr. Carron most recently served as Geology Superintendent for AngloGold Ashanti, where he helped advance the Arthur epithermal gold project in Nevada from discovery-stage exploration through resource development and into Reserve status; and

- Adding Depth to Team as Exploration Activity Accelerates: Mr. Carron joins Headwater as the Company ramps up exploration across multiple partner-funded programs and newly generated 100%-owned opportunities, including the Jupiter Project, a district-scale epithermal project where the Company is applying leading exploration concepts, some of which were used in the discovery of the Arthur project.

… Being able to attract this kind of highly relevant top talent is a good sign.

The Risk/Reward

This is simply one of the cleanest, asymmetrical Risk/Reward “no-brainers” that I am aware of. The team has proven how exceptionally good they are at spotting projects with legit, significant potential since they have a whopping #6 projects that have earn in agreements already with large mining companies. If we just take the activated Stage 2 earn in for Newmont Mining on Spring Peak for example it entails US$40 M (C$54 M) of spending which is higher than Headwater’s MCAP and not far from a double of the Enterprise Value. On top of that they would earn 10% in Management Fees. Since Newmont is a C$126 B company it goes without saying that they would not bother with any exploration story if they did not see multi-billion dollar potential (anything less wouldn’t really move the needle and be worth their time). I mean this is not me or some random dude on the internet saying that Spring Peak/Lodestar has multi-billion dollar potential, it is the largest gold mining company in the world Telling us.

Lets play around with a binary scenario where success would be Headwater proving up something worth $2 B at Spring Peak/Lodestar over the next four years (Note that this is not the Blue Sky scenario since there are quite a few examples of LSE deposits that would be worth a lot more than that at today’s gold price). Anyway, Headwater would be fully carried up until, and including, a PFS study which is the point where Headwater would keep 25% of the project plus a 1%-2% NSR. For simplicity lets say they would keep 30% of a $2 B deposit which translates to 0.3 * $2 B = C$600 M. C$600 M is around 20X what the current Enterprise Value is so at face value one could crudely suggest that this scenarios has a 5% chance priced into the stock all else equal. Personally I think Newmont would need to have higher internal conviction than that to execute Stage 2 but I digress (And this does not even account for scenarios where it could be worth more than $2 B even though Newmont obviously have higher hopes than that).

Lets just say that I think the easiest way to describe the asymmetrical Risk/Reward that I see in Headwater Gold is that I would argue that the company is most likely undervalued just in light of the Spring Peak project and earn in deal with Newmont. THEN you add Lodestar (Newmont), TJ (Oceana Gold), Hot Creek (Oceana Gold), Jake Creek (Oceana Gold), Crane Creek (Centerra Gold) and another six projects (and counting) on top of that which would not be priced in at all in that case. Furthermore SIX of these projects happens to be located in Nevada (USA) which has again claimed the #1 spot in the world on the most recent Frasier Institute rankings of global mining jurisdictions.

… Does one need to be a geologist, mining engineer, top notch analyst or even have more than some common sense to realize that the market is pricing it waaay too low since the marginal investor is notorious for being unable to price in anything more than the flagship project if even that? Now I can’t guarantee anyone will make money in Headwater Gold from these levels but there is no one on earth that can convince me that the Risk/Reward is so asymmetrical, in a positive way, that its hard not to laugh at Mr Market.

It’s like paying for one hand in poker but get to play 11 hands and 6 of the hands have major miner validation. Headwater and its partners needs to be wrong on 6 to 11, or even more, projects for Headwater to end up as a failure. On the flip side if ANY of these six major miner validated projects live up to the potential, or the other six wholly owned projects deliver, then Headwater is so lowly valued that a multi or even multi-multi bagger could materialize over the coming years.

Even if we assume a mere 10% chance of significant success at any of the six partnered projects then the odds of total failure (6 out of 6 fails) is 53.1% aka a 46.9% chance of success. And that significant success could be anything from a 4X to a 10X or more depending on the size of the success. And then account for the fact that the company will likely keep generating new projects and potentially generating new partnerships. This skews the Risk/Reward even more favorably and it also decreases the risk that this story can even end with a terminal failure anytime soon.

Note that the Risk/Reward of such a vast portfolio shines the brightest over a longer holding period where they get to kick a lot of cans. If ones investment horizon is only a couple of months or less then a lot of what makes this case almost unique is wasted.

The Beauty of Dilution/Inflation Protection in a multi-asset junior

In an interview I liked the way the CEO Caleb explained the beauty of the prospect generator model (Cash heavy earn ins in Headwater’s case) model- He points out that a junior that owns their project fully will still of course have to issue shares in order to explore and reach an economic study stage. Thus, maybe a junior that owns their project 100% and makes a discovery will have diluted the share count by say 40% by the time that an economic discovery and an economic study has been produced. Furthermore he highlights the fact that with these earn ins the dilution only happens in case of success. If a larger mining company fully carries and spends lets say $10 M to explore and then gives up the company suffers no dilution from that project. If it was 100% owned however a junior might have diluted itself by 25% on a corporate level in addition to suffering a negative outcome. In the earn in deals the (project) dilution only comes in case of success(!).

If we summarize these scenarios on a per project basis it means that Headwater sees no dilution in case the major miner spends their money to reach a negative outcome for the project. But in case of significant success Headwater would retain 25% plus a 1%-2% NSR which roughly translates to say 30% project interest at a PEA or PFS stage. The self funded junior, in case of success, might still only retain lets say 60% of the project at the same stages when accounting for dilution (Note that there are examples where a junior has been very successful technically speaking but the required dilution meant that early shareholders barely made any money).

Now consider these angles to a company like Headwater with multiple earn ins. For example lets look at two companies each with an identical set of four different exploration projects. Company A owns its projects 100% and company B has earn in deals on all four projects. If company A has a MCAP of $40 M and raises $10 M to explore their first project, and it fails, then the holders interest in ALL three remaining projects has been decreased by 20% etc. This means that failure at any projects has negative spill over affects for shareholders when it comes to the other projects as well. However, failure at any project for company B (the multiple earn in company) sees no negative spillover affects in that way outside. If its the fourth project that ends up being a significant success then company A might have already diluted shareholders by say 50% (100% share increase) by the time the discovery is made while company B has not seen any pre-success dilution while also enjoying kind of a capped, inflation protected journey to an economic study stage.

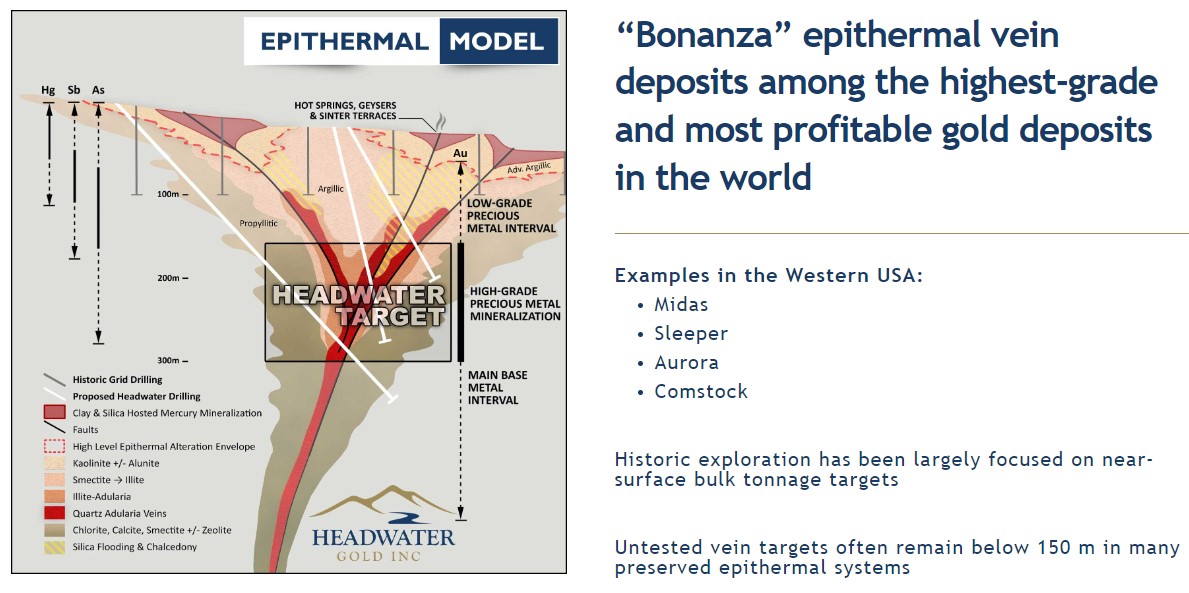

Setting the scene – Low Sulphidation Epithermal Systems

Headwater Gold was started with the goal of discovering high-grade, underground, lower tonnage (lower CAPEX), Low Sulphidation Epithermal (“LSE”) systems in Western USA (Tier one jurisdictions) that major miners would want (Especially in this day and age of rampant inflation).

Low Sulphidation Epithermal Systems:

I find that quite few investors fully understand these types of deposits but thankfully they can be extremely valuable. There are historic examples from Nevada like the Sleeper mine, the Comstock lode, Midas and the Aurora mine which is literally right next door to Headwater’s Spring Peak/Lodestar project. More modern examples are the monster Silicon-Merlin (Bulk mine), Hishikari and Las Chispas to name a few.

What is the reasoning behind this goal?

- Lower tonnage & likely underground -> ESG & permitting benefits

- Lower CAPEX -> Lower risk in a high inflation and higher rate environment

- High-grade -> Potential for good margins (value) even in a high inflation (cost) environment

- Western USA -> Nevada is ranked #1 in the world which means a premium on any success

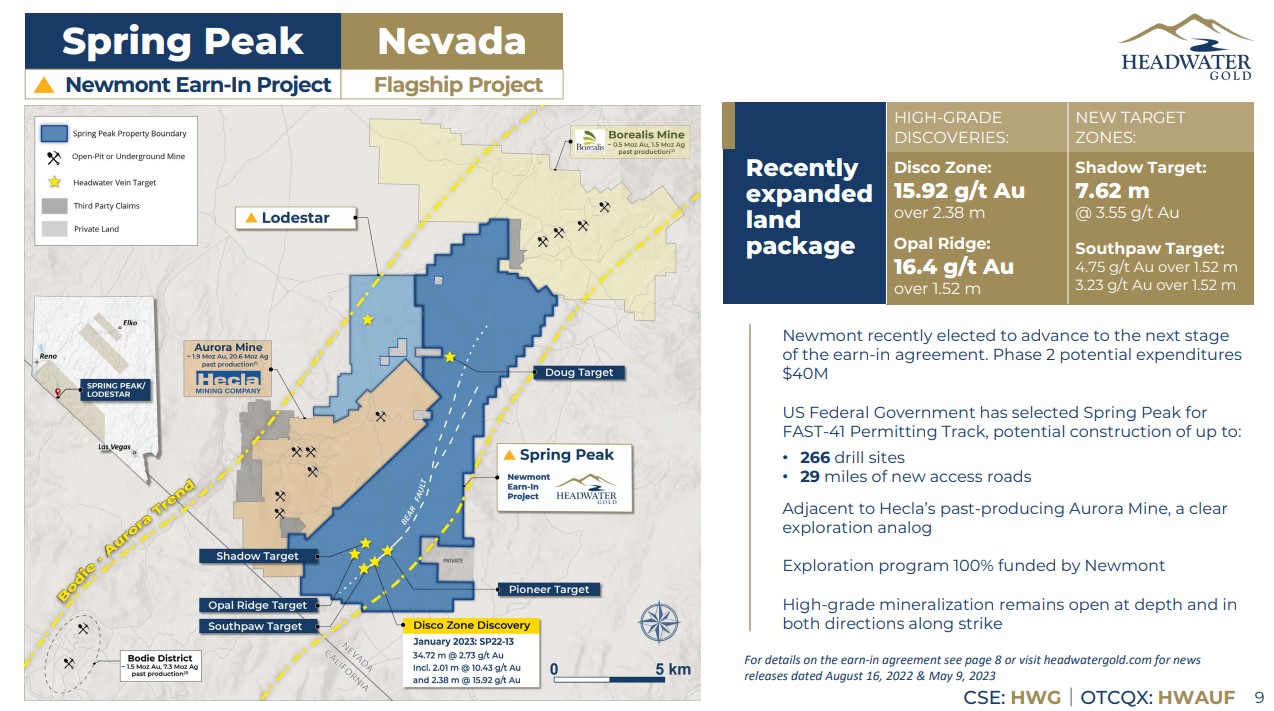

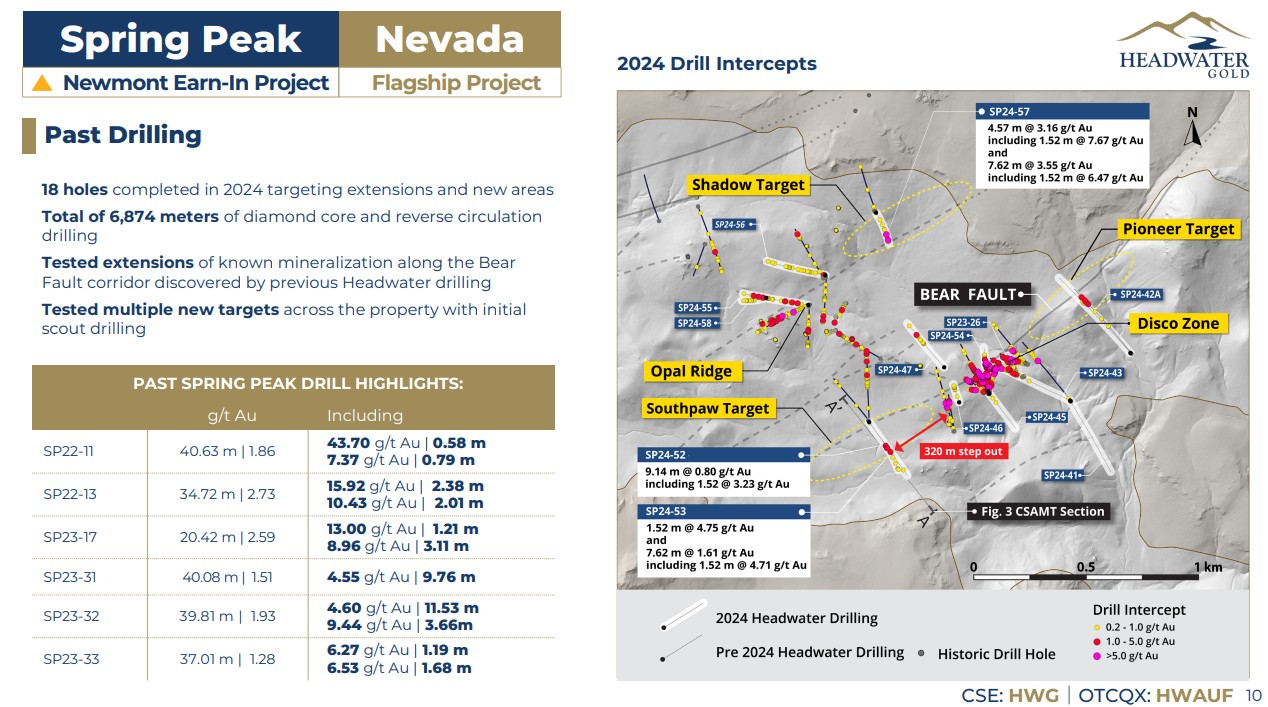

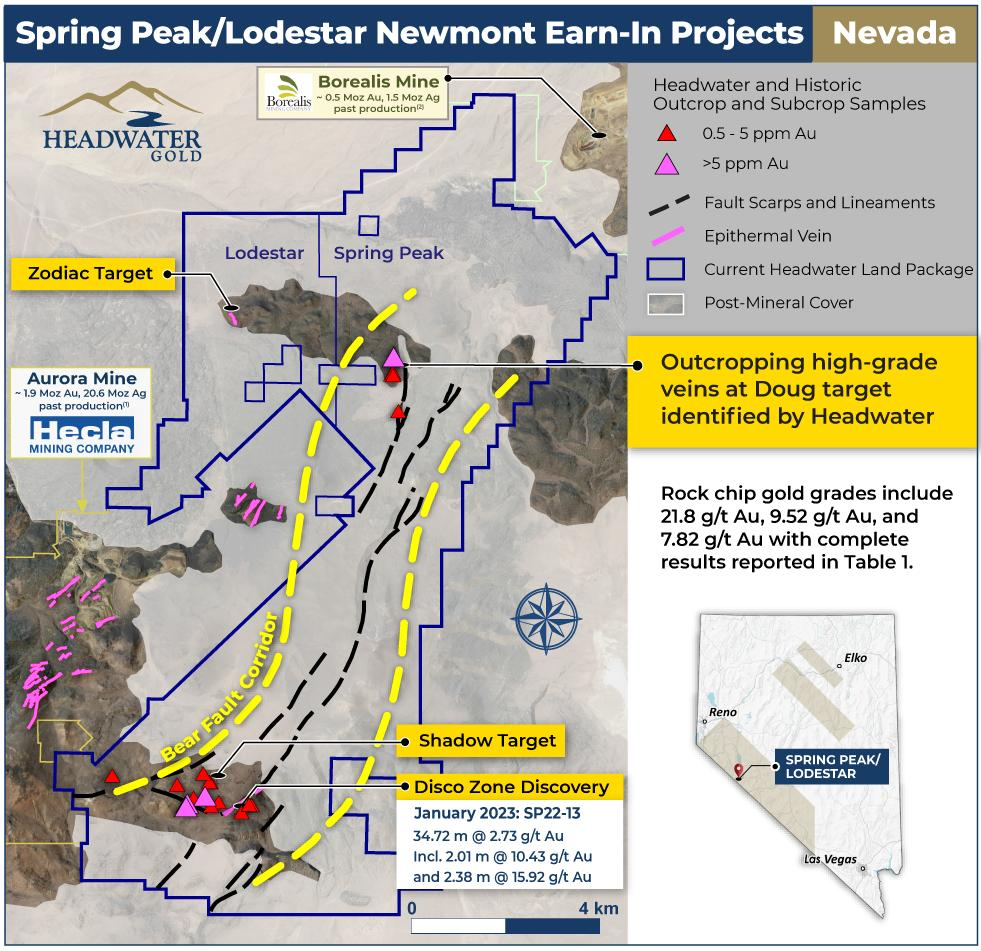

#1 “Spring Peak Project”, Nevada (Earn in with Newmont Mining)

The Spring Peak project could be considered to be the flagship project for Headwater Gold because it is the largest earn in, with the largest gold miner in the world, and discoveries have already been made at different targets:

As with any multi-asset junior the market typically only makes you pay for the flagship project since Mr Market has a very hard time to have more than one thing at the front of its mind at any point in time. The interesting case with Headwater is not only the sheer amount of project one gets “for free” but also that right now the flagship project is considered quite boring due to lack of news recently. In essence I believe that Headwater is pretty much only pricing in a discounted Spring Peak project with an enterprise value of around C$29 M. This combination is, in my opinion, the biggest reason for why I think its so absurdly undervalued and sports one of the most asymmetrical Risk/Reward propositions of any early stage explorer I have come across over the last 10 years. The thing is that Spring Peak has been boring lately is because the project was selected for FAST-41 permitting track by the US Federal Government so Headwater and Newmont are simply waiting for this to conclude so the exploration can pick up for real. As one one can read in the slide above the potential for 266 drill sites and 29 miles of new access road is waiting at the end of the tunnel…

Assuming this FAST-41 concludes in a positive manner then the flagship project could go from Neutral to Gear 5 in a hurry. This is probably the most obvious revaluation catalyst since it is directly tied to the only project the market even slightly cares about (prices in) at the moment…

And contrary to the market’s current lack of excitement there is a lot to be excited about at Spring Peak as we can see in the slide below. Headwater/Newmont have already confirmed bonanza grades discoveries at two targets; Disco Zone: 15.92 gpt over 2.38 m, Opal Ridge: 16.4 gpt over 1.52 m, and high grade gold has been confirmed at Shadow Target: 3.55 gpt over 7.62 m, Southpaw Target: 4.75 gpt over 1.52 m.

Furthermore the company was able to find literally outcropping epithermal quartz veins a whopping 9 km to the north of the Disco Zone discovery at a new target called the Doug Target. These veins outcrop in a small erosional window which makes one (And Headwater/Newmont) think what might be hidden underneath that 9 km stretch of cover:

(Note that the Aurora veins and the discoveries made by Headwater Gold so far are all in erosional windows)

The highlights of the “Doug Target “are described as follows:

- New High-Grade Veins at Doug Target: Outcropping epithermal quartz veins have been sampled at the Doug target area, returning exceptional gold grades including 21.8 g/t Au, 9.52 g/t Au and 7.82 g/t Au;

- Bear Fault Corridor Emerging as a District-Scale Structure: The Bear Fault hosts Headwater’s high-grade Disco Zone 9 km to the south of Doug and remains open and untested by drilling under shallow cover between the two target areas; and

- Preserved Epithermal System: Vein textures and geochemistry at Doug indicate a high-level position within an epithermal system, suggesting potential for a preserved high-grade vein target at depth.

District Scale, Billion Dollar Potential

In the slide above one can see the vein footprints within the historic Aurora mine complex that is owned by Hecla today. If one found another Aurora type complex today it would probably be worth a few billion dollars. And that billion dollar potential was found just in erosional window areas of this district. As for Headwater the starting point today is also discoveries made at Spring Peak within an erosional window in the southern part of the land package and I think one can expect all of these zones to grow with more drilling. Personally I think the known targets will have material value thanks to the strategic location even if they do not result in a new Aurora type complex (or even half of an Aurora type complex) given that Hecla Mining still has a mill there and is also exploring:

Newmont is of course looking for a multi-moz, multi-billion dollar gold district but needless to say the threshold for economic success for the projects as a whole might be as low as it gets since even when all is said and, done only a small discovery is made, it could still be something any of the neighbors would want to mine. I mean even 200,000 ounces of high grade gold has a gross value of 940 MUSD and if one does not need to build any infrastructure really then that

With that said it is obviously the district scale potential that makes the largest gold company on earth to be excited. And the district scale potential is pretty obvious when one notes that the erosional windows have generated a multi-billion dollar prize in today’s dollars (Aurora), multiple discoveries have been made by Headwater in the southern part of the Spring Peak project in another erosional window, and there is 9 km of potential under cover between the Disco Zone and the outcropping Doug target.

Spring Peak Risk/Reward

- Most de-risked Headwater Gold project given confirmed low grade, high grade and bonanza gold intercepts at multiple targets

- Lowest threshold for monetizable success given proximity to Hecla Mining’s Aurora mill and Borealis Gold’s mine

- Some of the highest Blue Sky potential given the size of the project, Aurora mine proof of concept, and immense under cover potential between the Disco Zone and the Doug Target

- This claim is validated/confirmed by Newmont Mining’s interest

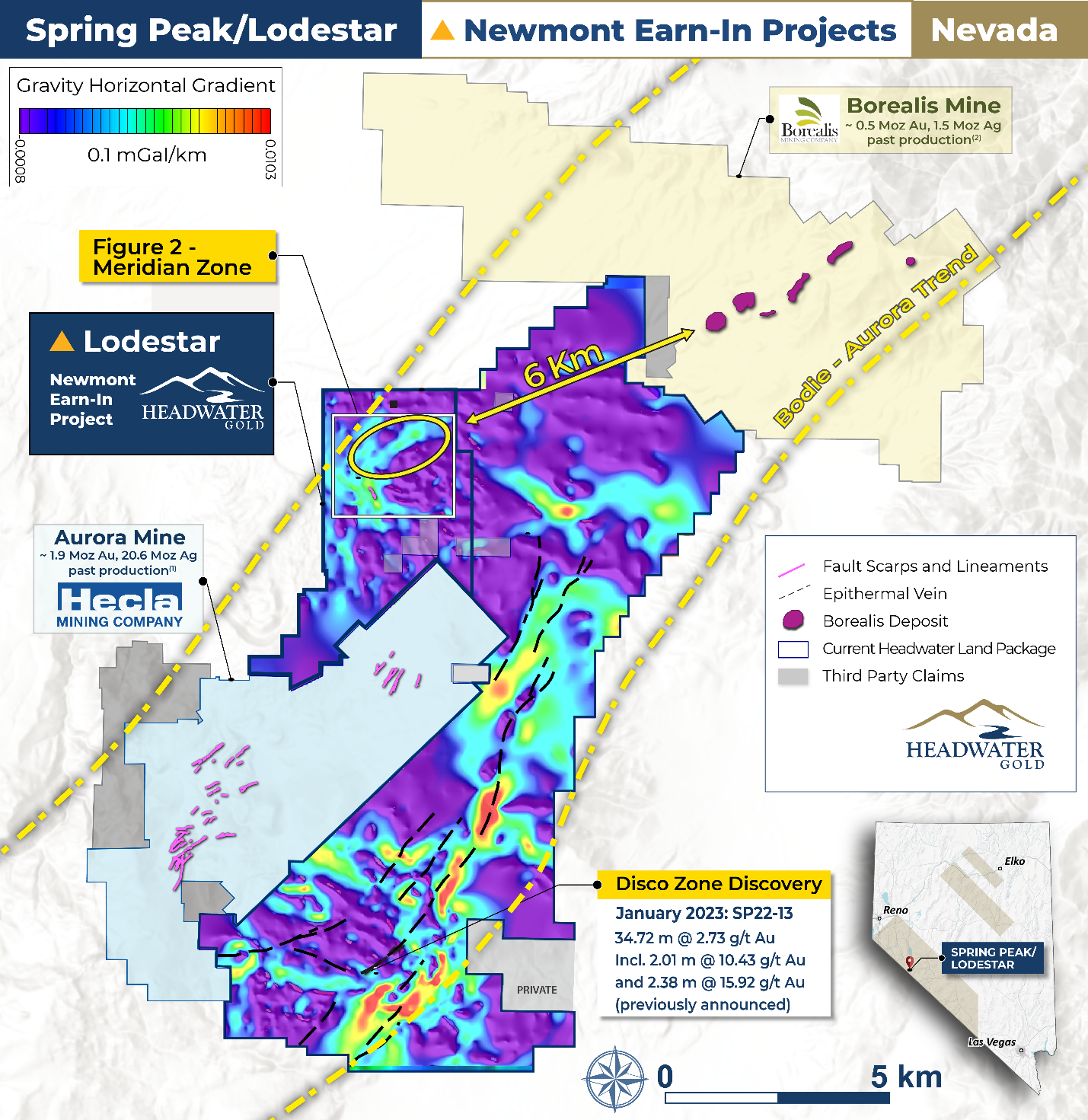

#2 “Lodestar Project”, Nevada (Earn in with Newmont Mining)

The Lodestar project adjoins the Spring Peak project and is on strike from Hecla Mining’s Aurora Mine and Borealis Mining’s Borealis project as can be seen in the previous pictures as well as below. Obviously this is not necessarily a stand alone project but rather an addition to, and included in, the Spring Peak district.

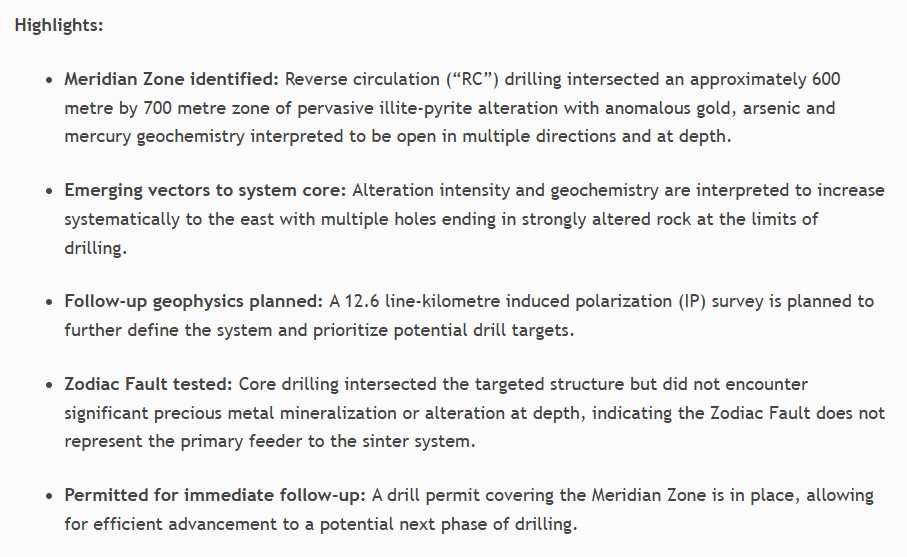

Headwater (Newmont) just released the findings from the first holes out of Lodestar and the highlights were as follows:

… Basically it seems that there is a lot of hydrothermal alteration at Lodestar, in the direction of the Borealis mine, and the company has planned to do additional geophysics with this new information. Headwater is permitted to drill more so another round of drilling could probably be expected as soon as the geophysics are done and interpreted.

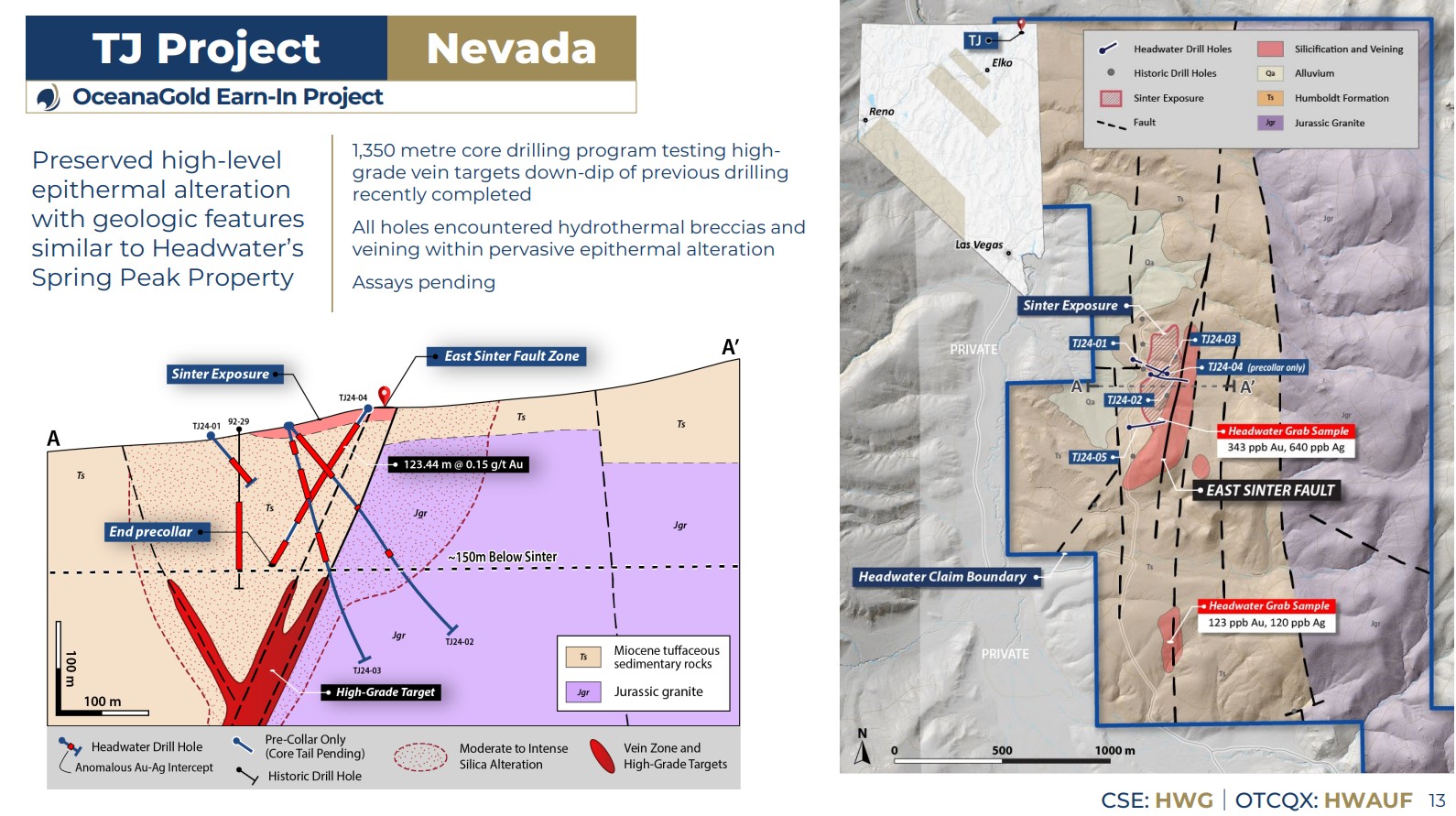

#3 “TJ Project”, Nevada (Earn in with OceanaGold)

The TJ project was staked a while back and the land package and limited information on the target was as follows:

Headwater recently completed their first pass holes and the feedback was encouraging:

“Headwater Gold Hits Highest Gold Grades to Date at TJ Project, Nevada and Expands Land Position 88%”

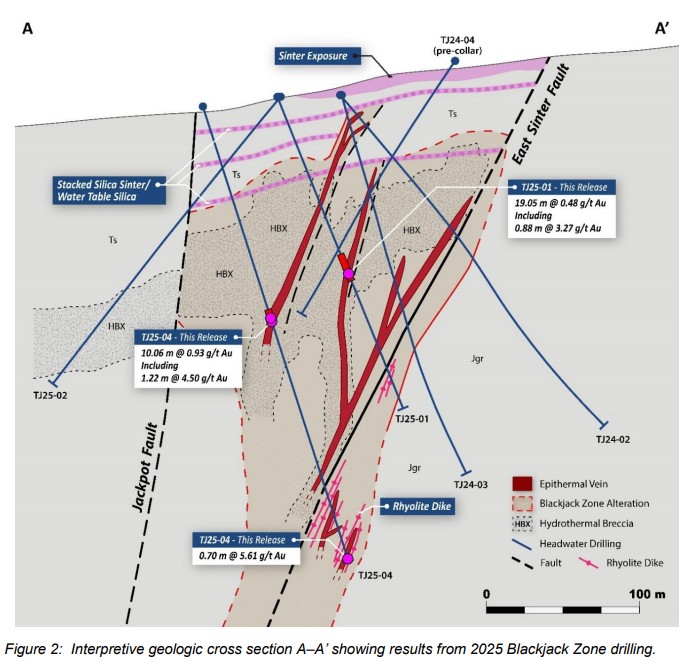

It seems there has been a very large amount of fluid flow at TJ as the news release suggest. Multiple, stacked sinter horizons (Shown in purple) were noted that points to this having been a long lived system with more than one episode of upwelling. We also learned that this limited drill campaign was able to produce the highest grade gold assays yet on the project. I am very interested in seeing what happens if they drill those veins again but intersect them at an even lower elevation since the 4.5 gpt and 5.61 gpt assays could signal that they are close to, or maybe even into, the boiling zone which is the main target/prize.

Caleb did an update interview for Kereport where he discussed the results out of TJ and stated that this drilling has confirmed that the CSAMT anomaly that showed a resistive body at that location does indeed line up with hydrothermal alteration. Basically it means that geophysics in the form of CSAMT looks to be efficient in outlining the mineralization at TJ. This is what excited the team as Caleb also explains that their limited CSAMT coverage only extends a bit north of the current drilling but the anomaly appears to be getting stronger in that direction.

Headwater Gold CEO Caleb Stroup discussing TJ:

Summarizing the recent findings at TJ

- Highest grades ever encountered at TJ

- Grades appears to be increasing with depth

- Vein widths appears to be increasing with depth

- Appears to be a long lived system with multiple sinter horizons and a lot of fluid flow

- The scale of what has been seen in drilling appears to be much more impressive than can be explained by the surface sinter expression

- The CSAMT resistivity anomaly appears to correlate with hydrothermal alteration

- The CSAMT resistivity anomaly is getting stronger to the north

Some quote by Caleb Stroup from the video:

“I still think we are just scratching on the edge of a very big system”

“We are seeing gold numbers increase with depth… Vein widths increase with depth.”

“This has transitioned from a very interesting surface anomaly of alteration to a very clear epithermal system that is very dynamic and at the scale that you want to see for a multimillion ounce gold potential bearing hydrothermal system”

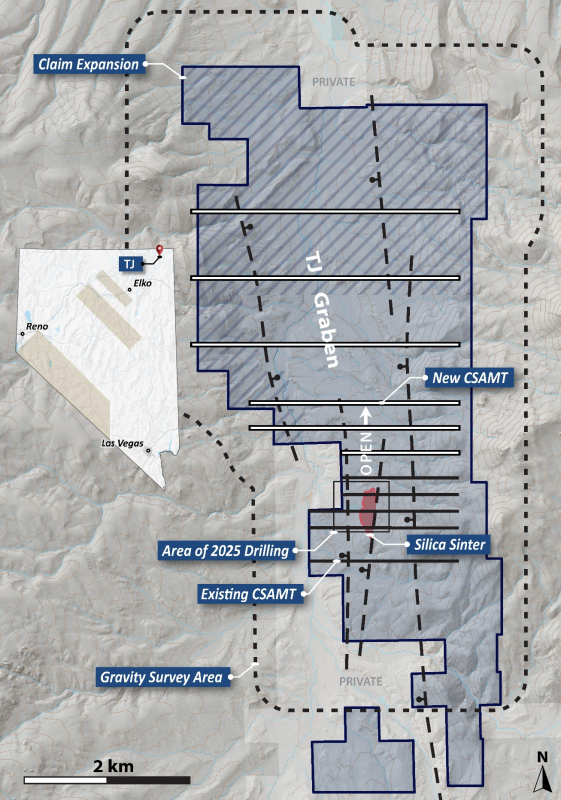

Obviously the company and their partner Oceana Gold have become more confident in regards to TJ’s potential as it was also announced that Headwater increased the land package at TJ by 88% in a northerly direction and just announced the plans for the extensive geophysics program:

What will be very interesting to see is what happens when they drill both deeper and to the north guided by the CSAMT results.

What the recent findings means for investors

- CSAMT appears to be effective so chance of drill success should increase

- The size of the potential prize at TJ has increased given what was seen in drilling coupled with the increased staking

- The odds of the next round of drilling delivering even better results has increased;

- CSAMT guided

- System appears to be getting stronger to the north (vectoring)

- System appears to be getting better at depth (vectoring)

My hope is of course that TJ turns out to be a district scale system(s) that ends up being worth… a lot.

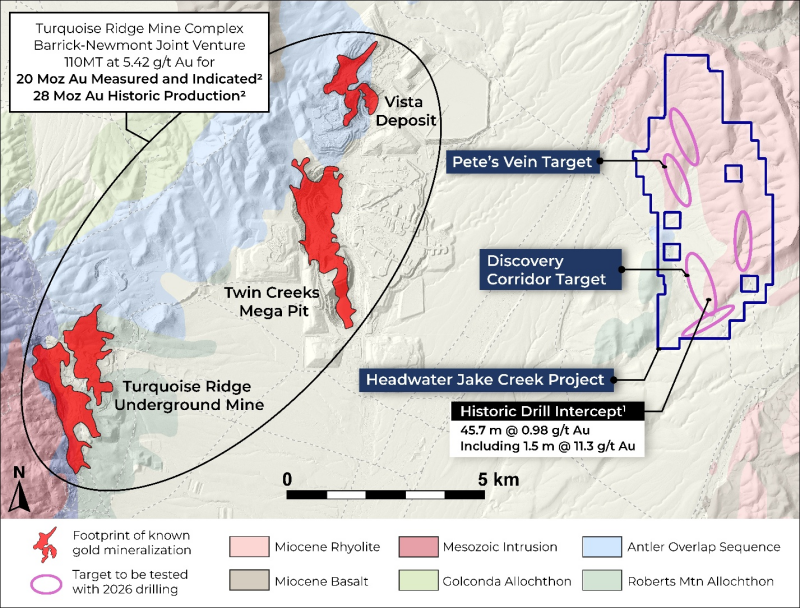

#4 “Jake Creek Project”, Nevada (Earn in with OceanaGold)

(Drilling now)

The Jake Creek project is a large scale, multi-target LSE project that has an exceptional location given that it is next door to an immense >>20 Moz gold mining district in Nevada:

Infrastructure is obviously exceptional and with such endowment it tells us that this area is incredibly rich in gold. Not only does the location lower the threshold for success, increases the value of any success, but also highlights the blue sky potential. Now, Headwater will focus on following up on the Epithermal mineralization that has been discovered and not focus on Carlin style gold, but regardless there simply is an enormous gold endowment here.

What I also really like, and I guess OceanaGold likes at Jake Creek, is that on top of all of the above this is already basically an LSE discovery already but it has simply not been followed up. Having hit grades up to 11.3 gpt gold over 1.5 m already confirms A) There is a LSE system present, B) It is precious metal endowed, and C) It can produce High-Grade mineralization:

Here is CEO Calep Stroup discussing the Jake Creek project and the now current drill campaign on Kereport:

Like pretty much every project outside of maybe Spring Peak I don’t really see any chance of success at all priced in for Jake Creek which I of course love from a Risk/Reward standpoint as an investor.

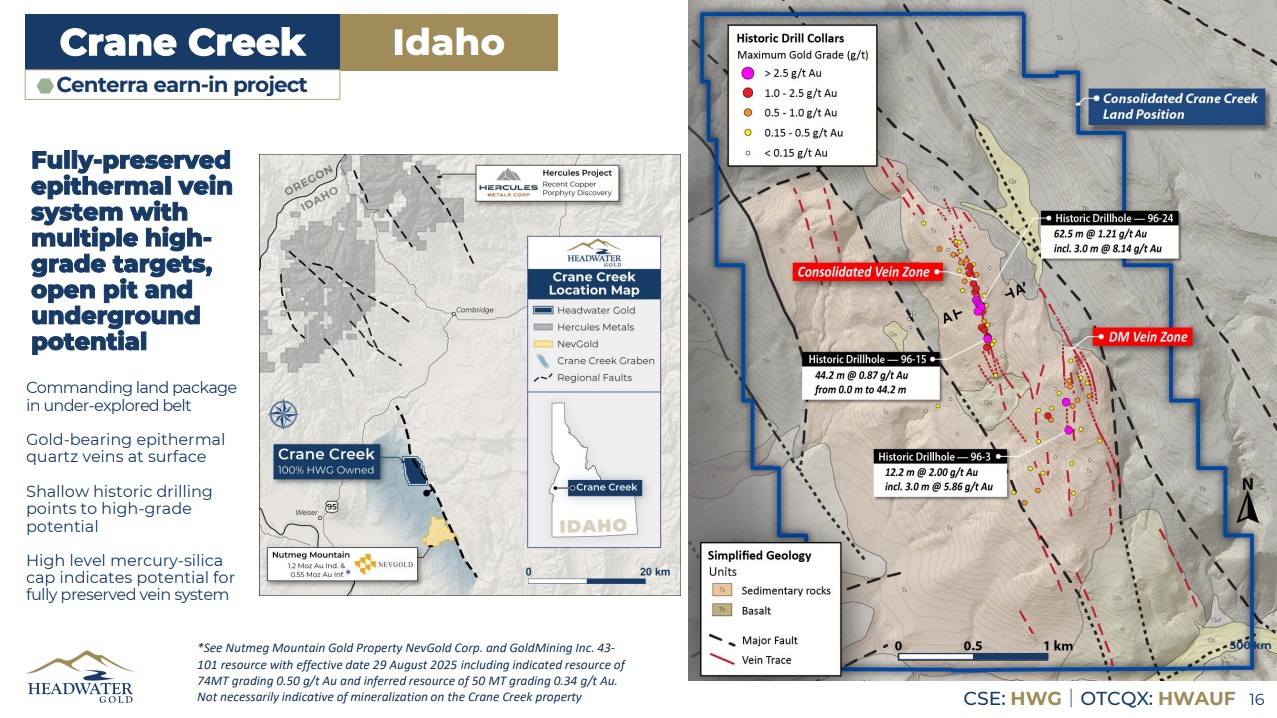

#5 “Crane Creek Project”, Idaho

The Crane Creek project is currently the only project which the strategic shareholder Centerra Gold has signed an earn-in agreement on. The project is not far from Nevgold’s (C$462 M MCAP) Nutmeg Mountain project and shallow historic drilling has already confirmed that there is an LSE-system present that can generate economic gold grades:

For Crane Creek the full earn in terms include Headwater getting fully carried up until the completion of a PEA on a minimum 1 Moz AuEq deposit at which point Headwater would retain 30% project interest as well as a 1%-2% NSR.

#6 “Rock Creek Project”, Nevada (Earn in with OceanaGold)

There is not too much information out there on Rock Creek but this is some information that be found on the project page:

Headwater’s land position adjoins private land and mining claims controlled by Nevada Gold Mines (“NGM”) and captures the along strike and down dip projections of the three principal vein systems in the district: the Main Vein, SW Vein and SE Vein. These principal structures occur within an approximate 5 kilometre (“km”) by 1.5 km epithermal alteration cell. An outcropping hydrothermal vent breccia cemented by chalcedonic silica in the center of the zone is interpreted as the upper parts of a well-preserved epithermal system. Historic rock sampling1 has returned gold values locally up to 34.2 g/t where the Main Vein projects south on to Headwater claims and the northernmost historic drill hole1 testing the Main Vein, also on Headwater claims, returned 27.43 m grading 0.89 g/t Au, including 4.64 g/t Au over 1.53 m suggesting strike potential in both directions.

Similar to Crane Creek there is already confirmation of a LSE-system that can generate economic grades. As with any project there are no guarantees of an economic deposit being outlined in time but there is a possibility it might happen and any of these projects could end up being a company maker.

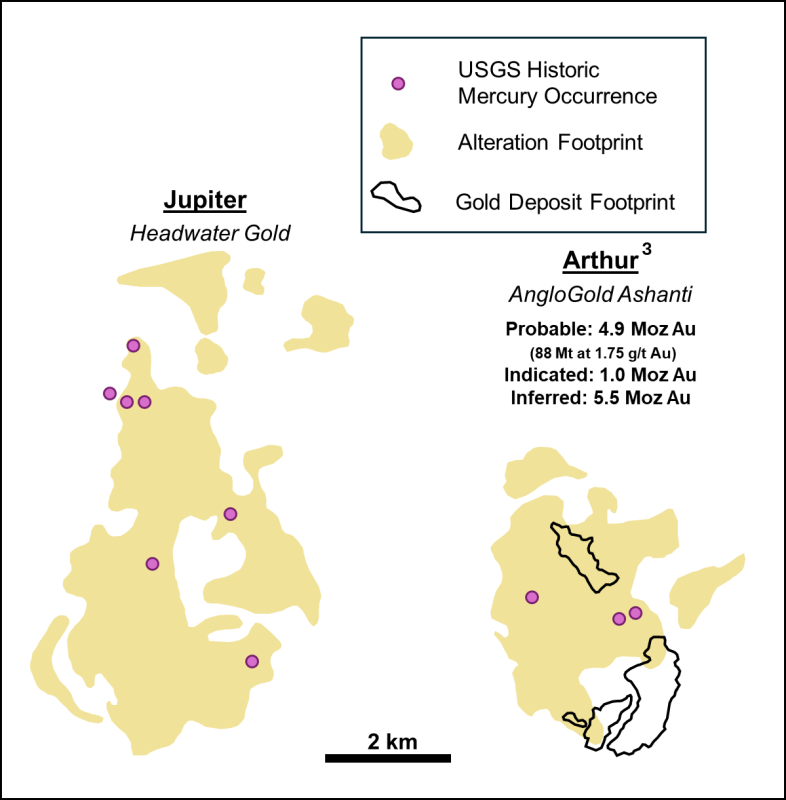

#7 “Jupiter Project”, Nevada (100% owned)

The Jupiter Project is the latest addition to the Headwater Gold portfolio and it hosts a very large alteration footprint in the Walker Lane region:

This is how CEO Caleb Stroup described Jupiter when it was announced it had been staked:

Caleb Stroup, President and CEO of the Company, states:

“Jupiter is exactly the type of opportunity we look for: a large, metal-bearing hydrothermal system in Nevada where previous work demonstrated the presence of gold but failed to recognize the scale and coherence of the system. Historical drilling confirmed the presence of gold mineralization, including 9.1 metres grading 1.1 grams per tonne gold associated with illite alteration, but that work was never followed up in the context of the broader mineral system. By compiling and integrating historical data with modern alteration mapping, geochemistry and structural interpretation, we now see a clear picture of a district-scale epithermal system with multiple structurally controlled targets which are untested at depth. We have secured a dominant land position across the full alteration footprint and have a clear path to systematically advance the Project.”

Jupiter is simply a huge target that might have nothing… But it could have something… Something very large. This alteration footprint comparison to the massive Arthur project was included in the news release:

I would not be surprised to see Jupiter be yet another early stage project that goes into an earn in deal with a major mining company. If not I assume it would be because Headwater feels that the Risk/Reward is good enough to keep it 100% and drill it themselves. Regardless I think this is yet another project that basically comes as “free optionality” to shareholders and it certainly has the scale to be something potentially significant.

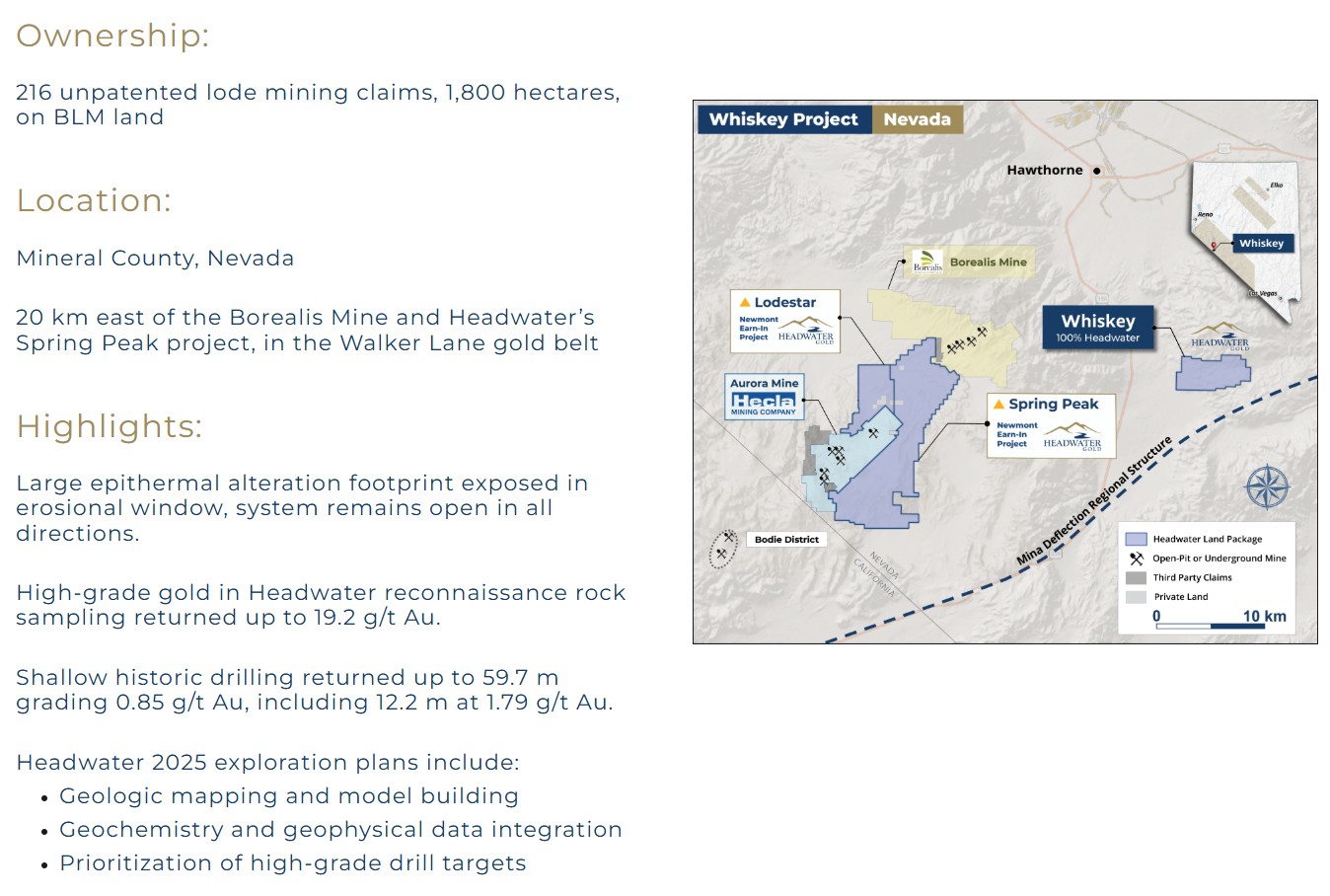

#8 “Whiskey Project”, Nevada (100% owned)

The Whiskey project is of the most recent project additions. Interestingly it is not that far away from Spring Peak and Lodestar as one can see in the picture below. This opens up some indirect synergy value in my opinion. Also the project has seen shallow historic drilling that hit up to 59.7 m at 0.85 gpt so there is already proof of concept that this LSE can generate economic gold grades.

A zoomed in view of the Whiskey project:

… If no stand alone deposit could be discovered here I reckon even a smallish high grade discovery with some hauling potential to the Spring Peak area could result in real monetization.

Other Projects

There are four additional projects, that we know of, in addition to the one mentioned above but in order to not make the article even longer I will not go through them here.

Closing Thoughts

At an C$32 M Enterprise Value I simply think it is incredible how much bang for the buck you get with Headwater. With at least 12 projects in hand, 6 already with major miner validation, the company needs to be “lucky” once for Headwater to potentially be a multi-bagger from here. In practice I think Spring Peak cover the entire market cap and I am just waiting for the FAST41 to go through so Newmont/Headwater can “carpet bomb” the project with drilling. With that scenario more ore less underpinning the case until further notice I think all the other ventures, and any new future ventures, kind of comes as free upside for the time being. I mean if/when Spring Peak gets the green light it could get very exciting even if they miss on every single project up until that point. The optionality then being that they might make a significant discovery before Spring Peak even gets into a much higher gear.

Amateur TA

As per usual it requires traders, algos, poor sentiment, weak hands, warrant clippers and other shenanigans to drives junior prices down to honestly offensive levels from a fundamental perspective. Fundamentally, based on Price vs my perception of the risk adjusted value, I think this will break higher:

Note: I own shares of Headwater Gold and the company is a passive banner sponsor so consider me highly biased. Always do your own due diligence and form your own opinions. Investing in junior miners can be very risky and never invest money you cannot afford to lose. This is not investing advice. I cannot guarantee the accuracy of the information in this article. I share neither your losses or your gains. Assume I might buy or sell shares at any time. I will not be able to hold anyone’s hands 24/7.

Best regards,

The Hedgeless Horseman

When do you expect the Whiskey Project to move forward?

I’m not sure L.B. The proximity to Spring Peak/Lodestar makes it interesting from a synergy perspective. With that said Newmont is probably slower than the mid tiers. In other words it might make sense for Newmont but maybe not on a standalone basis while it might make sense for mid tier/smaller major on a standalone basis. And there is also the option of drilling it themselves. Anyway, my simple answer is that I do not know when it will progress to drilling nor in what form.

All the best