THH – Some High Risk/High Reward Stories Testing Top Tier Targets

There are some big, good looking targets out there which ware being drilled right now or are soon to be drilled. I own shares of each companies mentioned and some are banner sponsors. None are major portfolio positions percentage wise. I prefer to be in a position where I can ride the stories higher without too much mental pressure to sell and rather in fact add on a discovery. The worst way to play these in my opinion is to have a nosebleed position going into maiden drill campaign assay risk (aka taking on high risk) and then selling a lot in case of success happening (High Risk for relatively Low Reward in practice). A safer way to play any of these is of course to simply have them on a watchlist and buy in after a discovery hole when the absolute upside is lower but in exchange the risk might be considerably lower as well by then.

Exploration aka Alpha risk has typically been my bread and butter. Thus I am glad to see developers/producers revalue higher which increases the relative Risk/Reward for explorers FINALLY.

I guess a characteristic that these juniors share is that that they all have A) exceptional flagship targets, B) skin in the game, C) that the management teams like their flagship targets so much that they have decided to test the targets themselves for maximum exposure (and maximum risk), and D) The targets are at surface, or believed to be near surface, which makes them junior friendly (Cheaper to test and lower threshold for success all else equal).

Anyone who does not like discovery risk could simply just add plays like this to the watchlist. The flagship targets of these juniors are so good/large that even if they hit, and go up 100%, the Risk/Reward could potentially be even better (Lower Reward but also Lower Risk).

Companies mentioned:

- Red Canyon Resources (Drilling)

- Kobrea Exploration (Drilling soon)

- Westward Gold (Drilling)

- Finex Metals (Drilling)

NOTE: Two companies just had news out in the last 24 hours; Red Canyon which stated it closed the financing and TECK ($26 B) is the “Multinational” taking a 9.9% stake and Westward Gold gave an exploration update.

Red Canyon Resources (REDC)

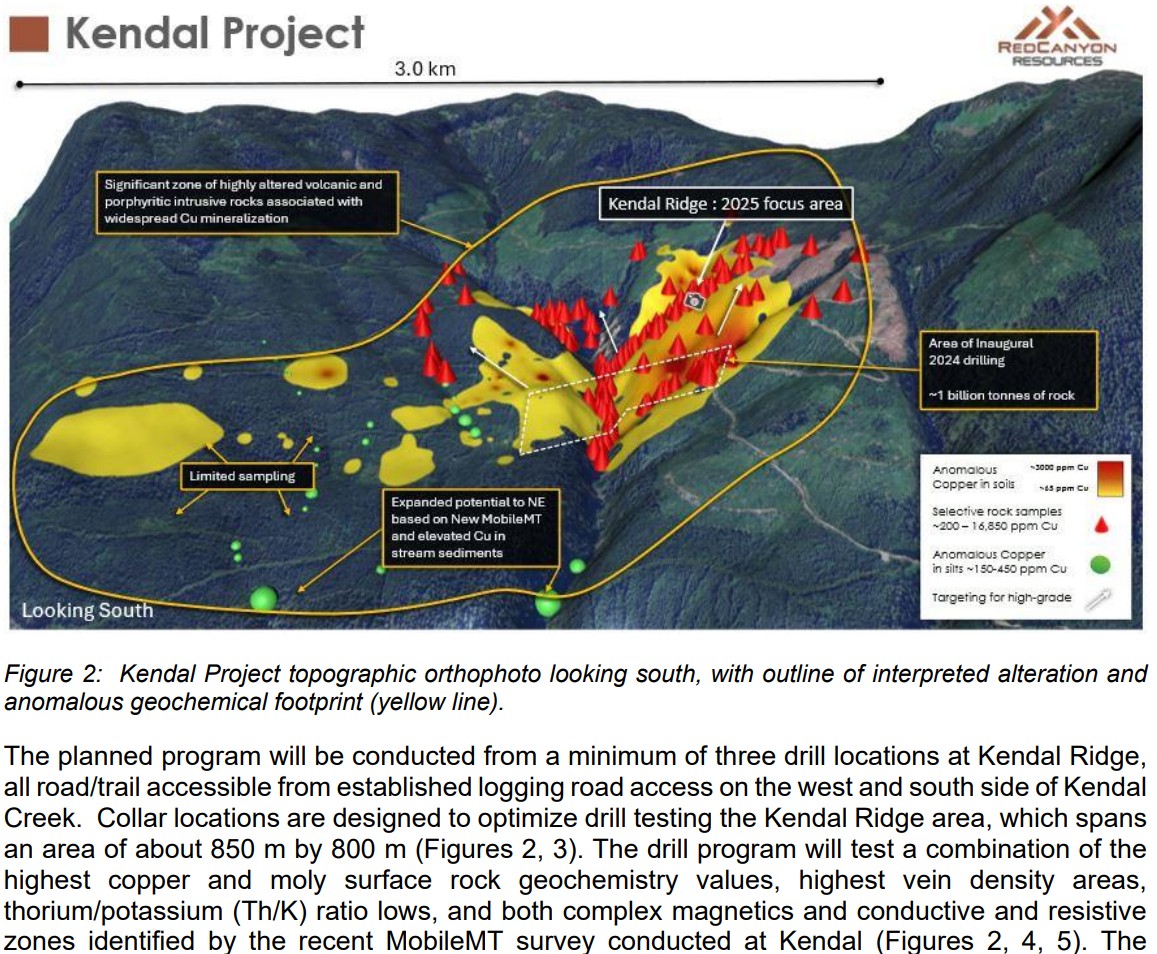

Red Canyon Resources which recently announced a Multinational Mining Company taking 9.9% of the company at a 94% premium just announced that the drill is turning at the massive Kendal project:

We do not know the identity of the Multinational just yet but since the drill is turning I would expect the deal to be closed surely and the entity to be known. I think it is safe to assume it will prove to be a multi-billion dollar mining company getting in. This then makes the asymmetrical Risk/Reward pretty obvious since Red Canyon will have a MCAP of around C$10 M while I would assume that the strategic investor coming into the company is looking for billion dollar projects. So the upside potential is material to say the least in case of success at Kendal. Red Canyon also have several more porphyry targets as back up which includes the massive Scraper Springs project in Nevada:

Is Red Canyon going to find one of perhaps many “sweet spots” at Kendal from this campaign? I do not know. I just know almost nothing of the sort is priced in and that I consider Red Canyon to have some of the highest upside potential in absolute terms of any junior I know.

Kobrea Exploration (KBX)

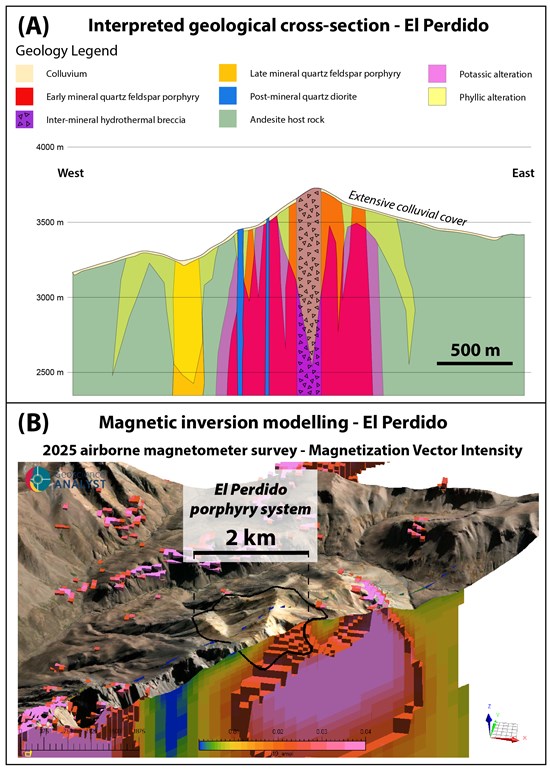

Kobrea Exploration also has a major flagship target in the form of El Perdido which is planned to see a drill rig for the first time shortly. Like Kendal the target is thankfully close to surface which makes it much more junior friendly. Success or Failure might be determined in the first ever drill campaign. Thus the campaign should be extremely impactful one way or the other… And this is a BIG target.

Latest description of the El Perdido target:

“The results of the airborne magnetometer survey support our interpretation that the El Perdido porphyry system is larger than previously recognized,” commented James Hedalen, CEO of Kobrea. “Our interpretation is supported further by the recently completed ASTER study that shows hydrothermal alteration extending to the east and southeast of the historically defined limits significantly increasing the size potential of this target that will be drill tested for the first time this upcoming exploration season.”

Kobrea also has a massive amount of targets in addition to the El Perdido project. In fact the company has 7 projects in total with a combined land area of 733 km2 which already includes multiple targets:

Just like Red Canyon it seems that the company wants to keep 100% exposure to at least El Perdido. I have no doubt there are many major companies ready to work with Kobrea in some shape or form on other projects so I consider them to have a plan B, C & D etc in case El Perdido does not turn into a company maker. With that said, assume heavy volatility depending on the results out of El Perdido since I assume that is the target which has the market’s focus.

Westward Gold (WG)

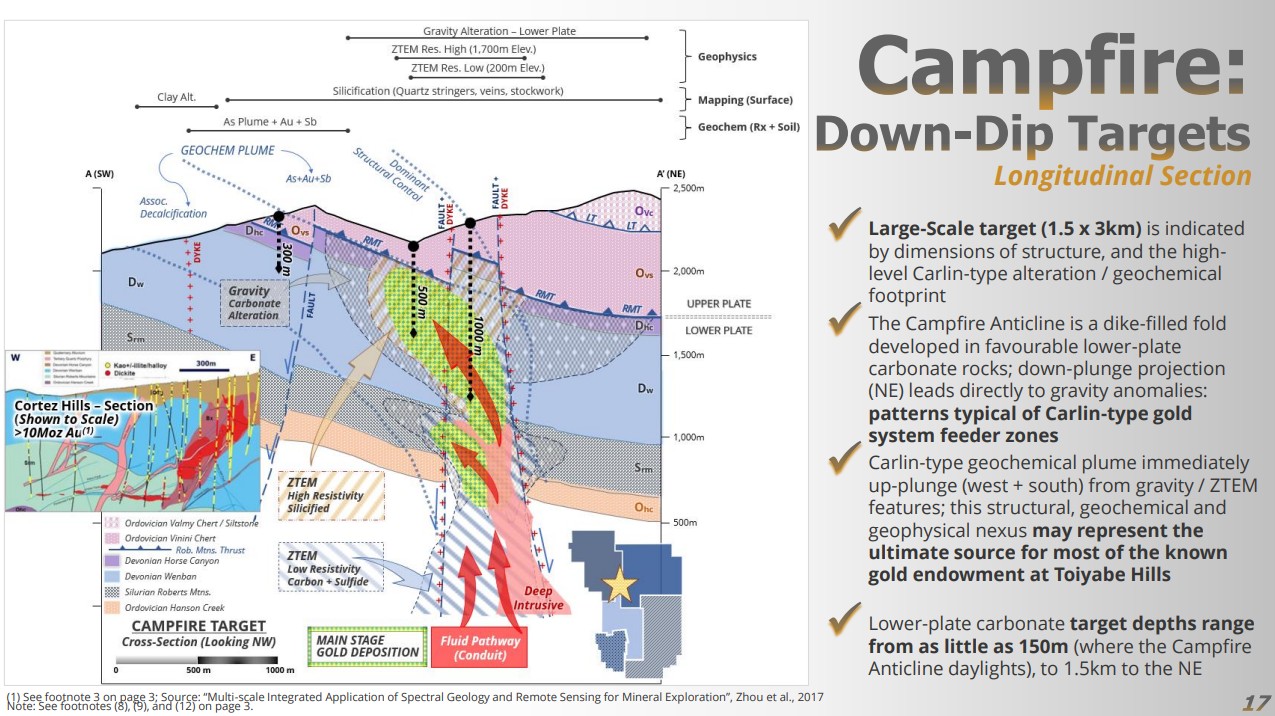

Westward Gold is another junior swinging for the fences in Nevada at their Campfire target where they are looking for a Carlin gold giant:

Description of the target:

Steven Koehler, Technical Advisor, added: “Having walked over and mapped countless acres of exploration ground across Nevada over the last 30 years, I’m acutely aware of the key ingredients which pique the interest of economic geologists and tilt the risk / reward calculus in our favour. Thru-going high-angle structures, igneous dikes, evidence of compressional events, hydrothermal alteration, outcropping carbonate rocks – these are the hallmarks of potential fertile gold environments. One or two of these may make a target, but seeing all of them in one place is exceptional; this is why the Campfire Complex currently has our undivided attention.”

The Campfire target is unusual because it is one of few Carlin targets left that is close to surface. A 5,000 m drill program is ongoing and first assays are expected soon. The company should learn a lot from these first holes to help them figure out where the ideal zones might be. I would be surprised if they hit a bullseye on their first tries but anything is possible. Like the other companies mentioned already I have no doubt that Westward could have easily made an earn in agreement with a Major miner but did not. Thus I think it says something about the team’s conviction (Higher risk for maximum exposure). The company has another project in Nevada but the Toiyabe Hills project which hosts the Campfire target is certainly the most important one.

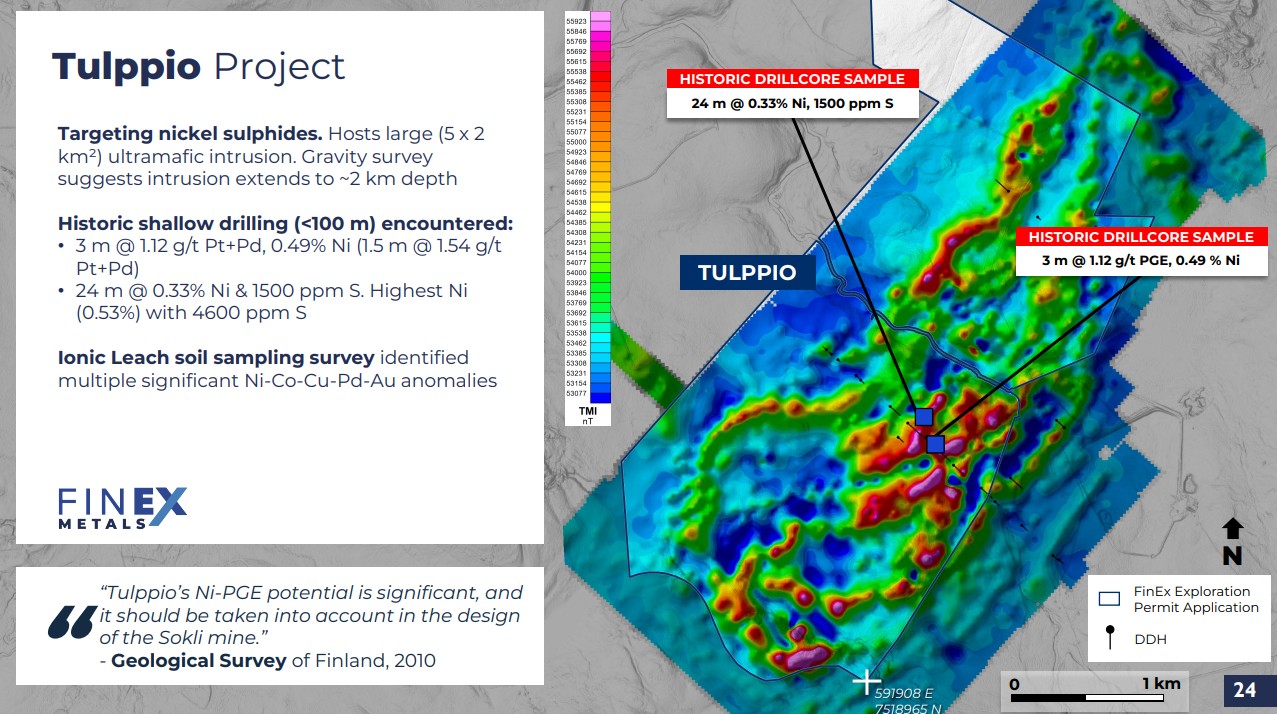

Finex Metals (FINX)

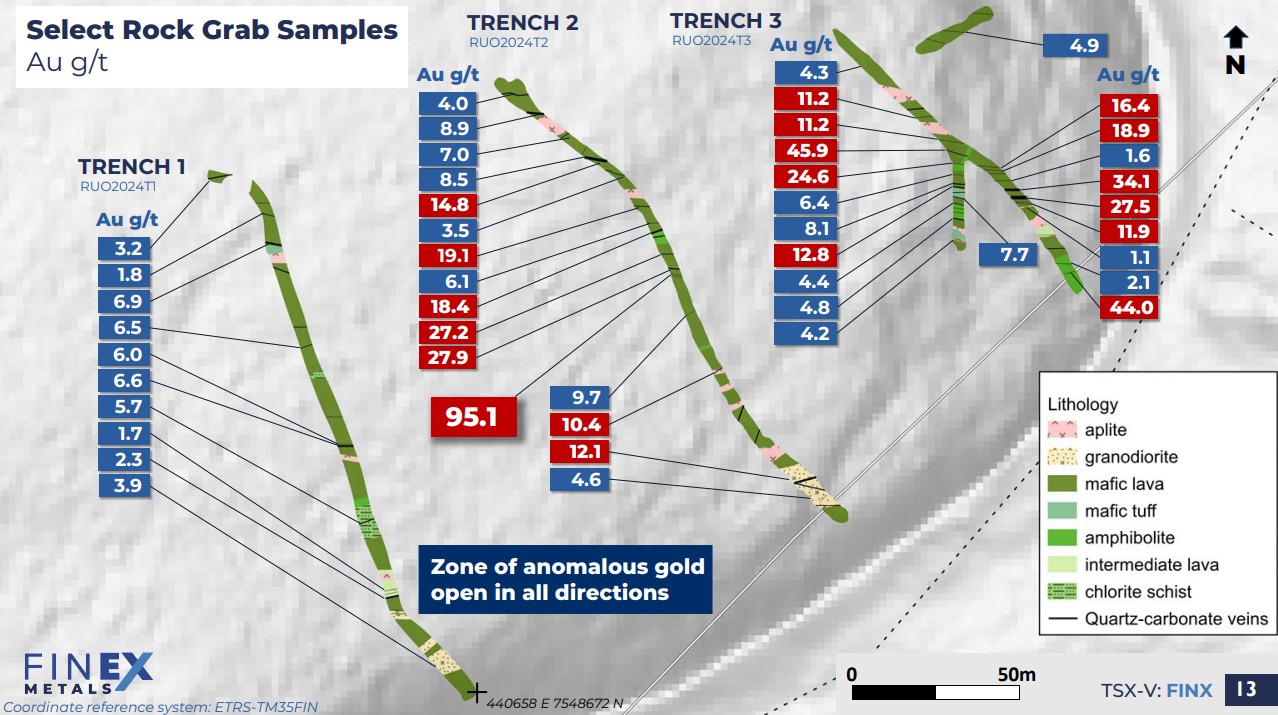

Finex is currently drilling their flagship Ruoppa project in Finland where the company found numerous gold bearing veins at surface after a trenching program:

What this target has going for it is that the mineralization starts at surface and that we already know there are mineralized veins that can produce very high grade gold. Thus it is a very junior friendly target so there is no surprise that Finex is drilling it themselves for maximum exposure. Given that this is by far the flagship target/project of Finex the coming assays, which are expected to come out soonish, will be very impactful. At a MCAP of C$22.7 M I think there is plenty of upside potential if this target turns out to be as good as it looks.

Finex does have other gold projects and the large Nickel/PGM “Tulppio” project so thankfully the case is at least not over in case Ruoppa would totally disappoint. Insiders own a lot of stock so they will be highly motivated to get a success elsewhere too.

Closing Thoughts

These are some of the best grassroot exploration targets/plays I am aware of right now from a Risk/Reward perspective. Again, the theme being that these all have so good looking targets that the insiders/management seem to willingly keep 100% of the exposure going into drill campaigns which I think says a lot. I have no idea what, if any, of these stories will make a significant discovery so I am not betting the farm on any. I have position sizes that will not kill my portfolio but could still have meaningful positive impact in case of success (+ time held). I am also very open to the possibility that I will be much more likely to add, rather than sell, in case one of these drill a hole(s) that suggests they are on to something very significant. A discovery story starts, not ends, with a discovery hole.

Pre-discovery plays should IMO not be large positions, percentage wise, in a portfolio. I think all of these stories have 10+ bagger potential but there is of course a risk that none of the targets will deliver anything meaningful.

Note: I own shares of all companies mentioned and some are banner sponsors as well so assume I am biased. Always do your own due diligence and form your own opinions. Investing in junior miners can be very risky and never invest money you cannot afford to lose. This is not investing advice. I cannot guarantee the accuracy of the information in this article. I share neither your losses or your gains. Assume I might buy or sell shares at any time. I will not be able to hold anyone’s hands 24/7. Juniors are RISKY!!!

Best regards,

The Hedgeless Horseman