My Simple Investing Strategy

My Simple Investing Strategy – Criteria I use

First of all I prefer to consider a longer term horizon than the market because companies with clear, near-term catalysts often gets bid up and companies with unclear and/or longer-term catalysts usually are trading at depressed levels. Second of all I prefer companies with enough internal growth potential to keep the market interested over many years and that is why my largest holdings are companies with either potentially very big projects and/or multiple projects. Thirdly, I don’t like the idea of a company going after a single small to medium sized project and potentially being forced to go out and buy a new project in a hot market. Fourthly, I prefer companies where management has serious skin in the game which should mean that the management team is not that interested in running a “life style” company where they are comfortable with just sitting around and doing nothing as long as they get their salaries. Lastly, I prefer companies that are not in the mature phase unless I really believe the people behind it can put their project into production because I don’t want to own a company where little can be done to increase value and excite the market and I risk just sitting around for years waiting on someone bigger to buy the project. Basically I want the people to be exceptional if I am to own a “mature” company where internal growth is either not a priority or is limited.

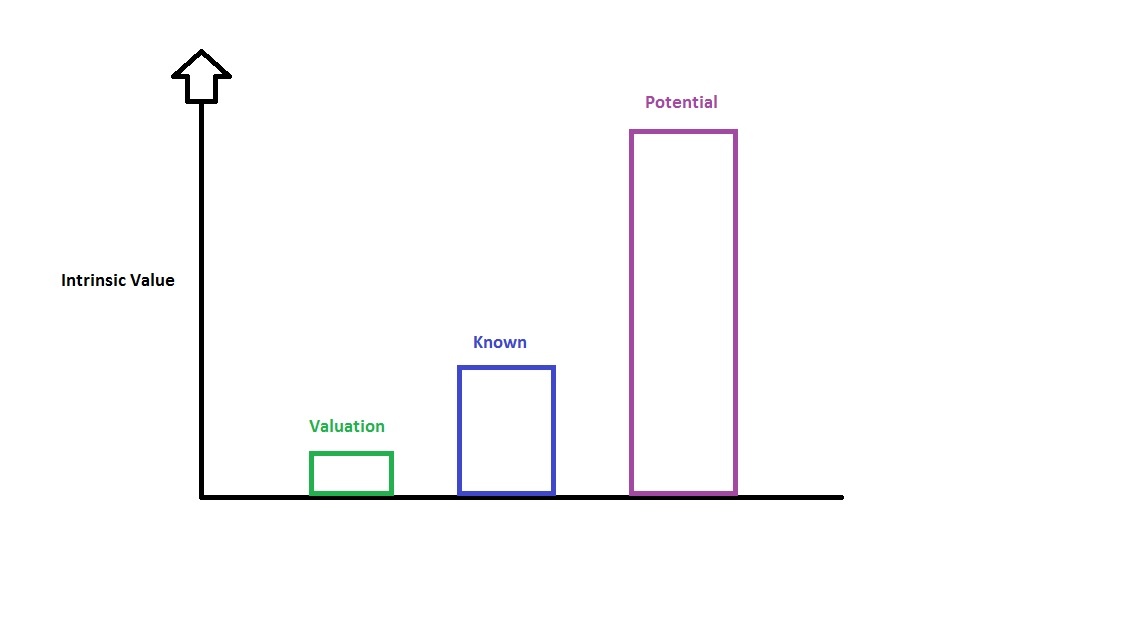

… In light of all that, I believe it opens up the possibility to both capture time-arbitrage (buying non-discounted future potential) as well as hopefully escaping a lack of news flow which might bore the market. If the market primarily discounts catalysts which are expected to happen within say a 3-month rolling basis then one would want to have a stream of expected catalysts on a maximum 3-month rolling basis, to keep the market from getting bored. Keep in mind that this theory assumes that one is fully invested and are not looking to take advantage of any dips due to the market getting bored. If the market does get bored and the company starts trading with an “impatience discount” then that is obviously a buying opportunity. I basically look for companies that are undervalued relative to what they already got and I get the growth potential for free:

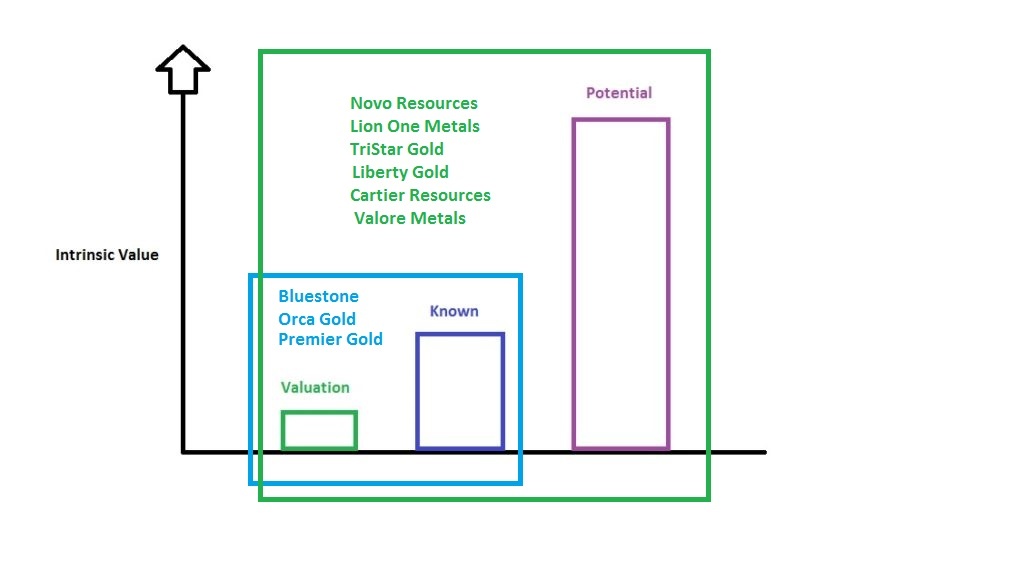

If I would categorize some of my holdings according to the graph above it would be something like this:

I for example left out Irving Resources because I consider Irving to be more of a pure potential play.

I truly believe in keeping things simple and if one gets the few important things right then half the battle is already won. I’m not a geologist or engineer after all…

In short I look for companies which fit most and preferably all of the following criteria:

- Skin in The Game

- Incentive to create actual value for shareholders

- Access to capital

- Being able to take advantage of the internal growth opportunities

- Internal growth potential

- Projects with significant growth potential and/or multiple projects in the pipeline

- Who cares?

- External validation

- Exception: If in the “mature” phase

- Company needs to have very good people with access to capital

Just to show you that I do indeed follow this “simple” strategy I thought I would go over some long term holdings of mine:

Irving Resources

- Insider ownership: Very good

- Management/Directors own 18.60% of the company on a fully diluted basis

- Access to Capital: Very good

- Eric Sprott

- Newmont Goldcorp

- Potentially Sumitomo Corporation

- Internal Growth Potential: Very good

- 4+ high-potential targets within their first claim block, The Omu Project

- One target is currently being drilled (Omu Sinter) and another is expected to be drilled this year as well (Omui)

- The Hokuryu and Maruyama targets are expected to be drilled next year

- … And Irving has several additional large projects in Japan

- 4+ high-potential targets within their first claim block, The Omu Project

- Who Cares:

- Newmont Goldcorp

- Sumitomo Corporation

Novo Resources

- Insider ownership:Very Good

- Management/Directors own 14.96%

- Access to Capital: Very Good

- Eric Sprott

- Kirkland Lake

- Sumitomo Corporation

- Internal Growth Potential: Unparalleled

- 13,000 km2 of land holdings

- Three potentially semi-basin to basin wide systems to explore

- Mt Roe conglomerates

- Hardey Formation conglomerates

- Egina type lag gravels

- Hardrock targets

- Talga Talga

- Blue Spec

- Who Cares:

- Newmont Goldcorp

- Sumitomo Corporation

- Kirkland Lake

- Creasy Group

Lion One Metals

- Insider ownership:Very Good

- Management & insiders own 22%

- Access to Capital: Good

- Been able to do multiple big financings throughout the company’s existence

- Good institutional backing

- Internal Growth Potential: Very Good

- Controls an entire Alkaline Gold system (very rare)

- 10Moz+ potential

- Starter project with very good economics for staged growth

- Who Cares:

- Quinton Hennigh

- I know some very large entities have visited the project in the last year (pending)

TriStar Gold

- Insider ownership:Very Good

- Insiders & associates own 27%

- Access to Capital: Good

- Recently got backed by Royal Gold

- Internal Growth Potential: Very Good

- Controls a whole paleoplacer “basin” that is 7-9km from side to side

- Already delineated 2Moz of resources just from drilling the edges

- A Tarkwa look-alike (Tarkwa is operated by Gold Fields and is a 30Moz+ paleoplacer deposit)

- Who Cares:

- Royal Gold

… I think I have made my point.

Some short notes on some other holdings that fit most of the criterias:

“Mature” companies with high insider ownership, excellent people involved and good backing:

- Orca Gold

- Big project in Sudan and a spin off in Ivory Coast

- Backing

- Resolute Mining

- Kinross Gold

- Lundin family

- Bluestone Resources

- Excellent project in Guatemala

- Lundin family owns 34%

Other Favorites:

- Liberty Gold

- Skin in the game

- Excellent people involved

- Loads of internal growth potential

- Backed by the Oxygen Group

- Great access to capital

- GFG Resources

- Skin in the game

- Excellent people involved

- JV with Newcrest

- Premier Gold Mines

- Skin in the game

- Huge pipeline of projects

- JVs with Newmont, barrick and Centerra

Companies with competent people involved that are just “too cheap”:

- Valore Metals

- Gatling Exploration

- Cartier Resources

- Genesis metals

I have more holdings that the one listed in this article but they are more speculative or are very mature producers already.

(Note: This is not investment advice and I am not a geologist. Always do your own due diligence. I shares of all companies mentioned, which I have bought in the open market and am thus biased. Novo Resources, Lion One Metas and TriStar Gold are passive banner sponsor on my site. )

Best regards,

The Hedgeless Horseman

Follow me on twitter: https://twitter.com/Comm_Invest

Follow me on CEO.ca: https://ceo.ca/@hhorseman