Stan Druckenmiller and Some Horseman Thoughts

Setting the Scene

Stan Druckenmiller is one investment legend that has influenced me the most I think. In the short clip below I see his investment philosophy as a mixture of Pareto’s Law (The 80/20 law) and “time’arbitrage”.

(HH: Notice the reaction of the crowd to some of his investing views. They laugh… That’s all you need to know about the herd’s mentality!)

Discussion

I prefer to 1) Bet heavy when I believe the odds are in my favor, because lets face it, great opportunities don’t come around all that often, and 2) Take advantage of the fact that most investors are impatient and seemingly seldom think of what a play will look like much further than say 3 months out, at best.

It is obvious that a lot of investors/speculators, especially in the mining industry, are short term catalyst hunters. When they learn that a potential catalyst is months or even weeks away, they sell with the intent to jump back in right before the said catalyst is expected. Since humans have a herd mentality and our body releases more dopamine the closer a potential reward could potentially be expected, one can assume that a lot of investors will OVER-discount the long term and UNDER-discount the short term. This means that often times (not always) the estimated Price/EV is cheaper (too cheap) when a stock is not expected to be able to potentially produce capital gains on the back of a catalyst in the NEAR future. At the same time, the human tendency to want instant reward makes it likely that a lot of people will want to buy a stock with prospects of a potential gain making catalyst in the NEAR future.

Theoretical example:

Lets assume that all else equal (before any material catalyst is announced) a stock “should” be priced at $1 based on long term expected value (EV). If the market (herd) does not think a catalyst is coming in the near future, and thus the stock is considers boring because the prospects of near future “rocket ship catalyst” looks bleak, the herd typically seeks to put its money elsewhere… The whole “everyone wants to get rich overnight” quote is a good description. So, lets say the stock is trading at a $0.70 because a big chuck of potential investors see no reason to be in it because they don’t envision getting rich quick anytime soon.

Then, 1) The company suddenly announces a week later that it will start drilling in the near future, and the stock trades up to $0.80 in a matter of days. A week after that the company announces that the drill rig hast started to turn on a “juicy” prospect, and the stock trades up to $1.10. Now, three weeks after that, the word has spread and the hype train is in full swing, and a bunch of people envision a stellar hit and the accompanying life changing gains. The stock is is now up to $1.50, with no material changes being announced yet (The geology is still the same that it was 2 months and 2 years ago).

Thus, we can conclude that although no material changes to the company has been announced, the market has drastically re-priced the share. This goes against classic economic theory since the share price and thus the company valuation “should” reflect the long term discounted cash flow or my preferred term, Expected Value (EV). The only thing that really changed between the announcement of a coming drilling operation and four weeks later is that the WAITING period for a POTENTIAL high impact catalyst was getting shorter by the day. In other words; With every passing day, the prospect of life changing gains draw nearer and nearer, which means the PRICE in terms of patience got lower and lower.

… Now think about that scenario fora bit. I would say that the two most important human factors that created the significant change in share price was 1) Impatience and the human lust for immediate reward, and 2) Greed.

A rational person or robot with the perfect knowledge that the EV of the stock was $1.00 would of course have bought when it was trading at $0.70 all the way up to $1.00, and then sold when it was trading above $1.00 since NO MATERIAL CHANGE to the company’s prospects was yet known.

Situations like this are seen ALL THE TIME in the mining space, and is probably the easiest form of alpha. The only catch is that it’s one of the hardest things to do, since we are all human and suffer from the same urges.

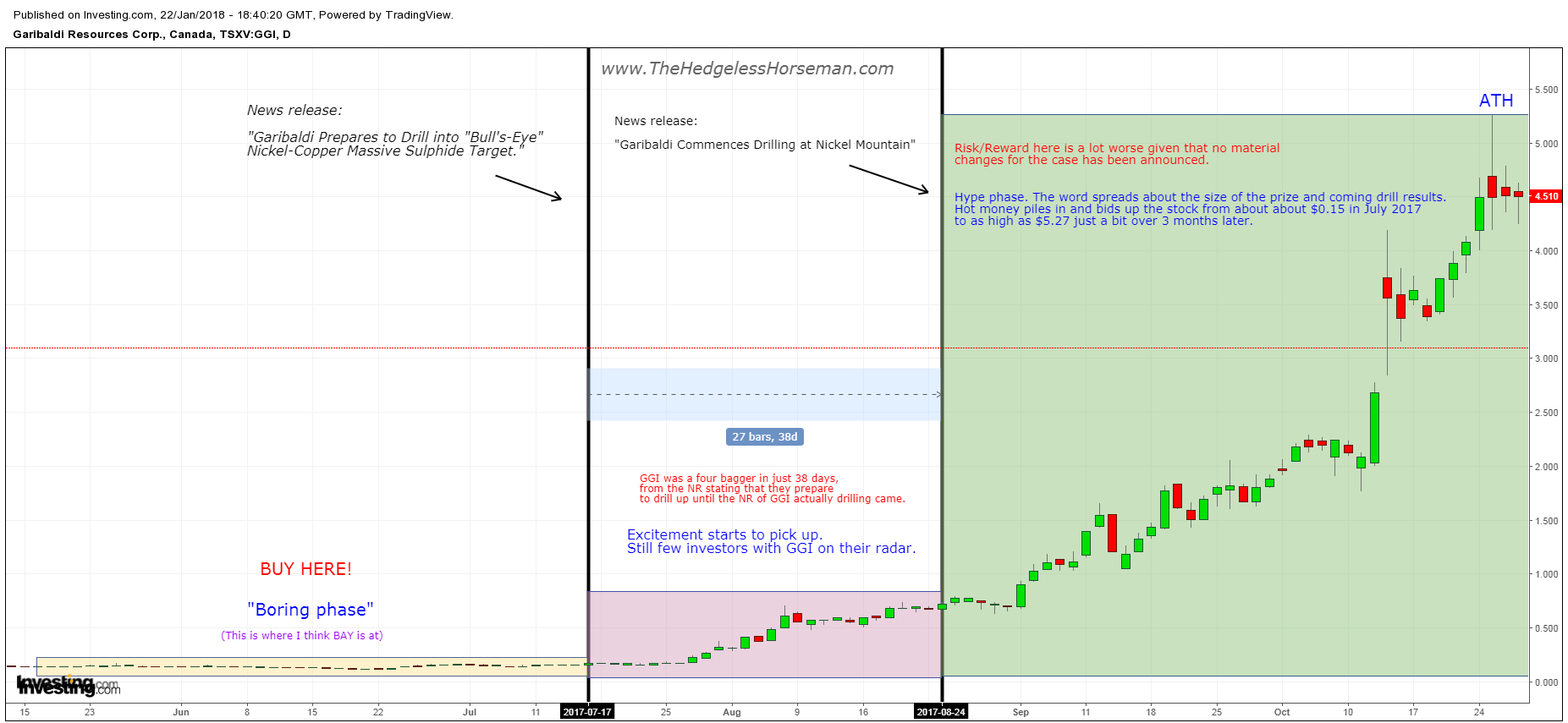

One of the absolute best examples of this in my mind is Garibaldi Resources (GGI) which I covered in THIS article when I was discussing the topic of time-arbitrage:

GGI – (CLICK to enlarge!).

Not only is it hard to stay disciplined and buy when no one wants to own it, one has to sell when others are piling in. Furthermore, it’s impossible to know just how “irrational” the herd could become. I personally sold out at $0.78 already(!), which was of course a big (short term) mistake in hind sight. If it was a mistake in the long term, one can’t know yet. I simply had done too little DD on Garibaldi to know if the rise in share price was warranted based on Expected Value, or if the share price had already priced the company above Expected Value.

Novo Resources is another case of an impatient market at works in my opinion. Every delay, no matter how small, has been heavily impacting the share price during the last few months. Catalyst hunters have become worn out and many have probably simply given up since it “feels” like news will never come.

Since I have done more DD on Novo Resources than any stock I have ever owned, I am of the view that Novo is undervalued based on my Expected Value estimations for the company given the CURRENTLY known information. This allows me to hopefully not do the same mistake that I (potentially) did with GGI, namely selling out because I had no idea what the Expected Value might be for Garibaldi and I got anxious that I might have overstayed my welcome when it started to run.

This also leads in to what Stan Druckenmiller said about envisioning what an asset might be worth 18-24 months from now, if not longer. A lot might change in 18-24 months, but that is for material changes to affect and for us to evaluate.

The companies I love are the ones I think are severely undervalued based on Expected Value (long term) and preferably companies I think are severely undervalued just based on what I think will take place in say a coming six month period.

In Essence:

See the future early as per Eric Sprott, and buy the case early, because the closer the story gets to “get rich quick” events, the more catalyst hunters will be bidding up your stock regardless of the Share Price/EV. In the case of Novo my personal belief is that we would need to rise substantially before the Share Price/EV is trading above 1.0.

Best regards,

The Hedgeless Horseman

Follow me on twitter: https://twitter.com/Comm_Invest

Follow me on CEO.ca: https://ceo.ca/@hhorseman

Don’t forget to sign up for my Newsletter (top right on front page) in order to get notification when a new post is up!

If you want to learn more about Novo Resources and the Pilbara Gold Rush you can purchase all my premium content HERE.

If you find my work valuable and want to help me keep publishing most of my research for free then please consider making a donation.