THH – Altamira Gold (ALTA.V): Going For a Multimillion Ounce Gold District in Brazil Backed by Aura Minerals ($3.5 B)

Sept 17, 2025

Altamira Gold is a gold developer/explorer which I think has changed tremendously for the better in the last year or so and the latest news release suggests their newest target could get quite a bit bigger. The company has three very large projects in Brazil but in this article I will focus on the flagship project called “Cajueiro” which also hosts both the Maria Bonita and Cajuiero Central gold deposits. I own shares of Altamira, and have been adding after the latest news release for myself and family members, so consider me biased. The company is also a passive banner sponsor so consider me twice biased. This article will be forward looking and speculative. This is not a buy or sell recommendation. Do your own due diligence and make up your own mind.

Altamira Gold in Short

- Margin of Safety

- 1.4 Moz of total, near surface resources with excellent infrastructure

- Upside

- Expand Maria Bonita, Cajueiro Central and numerous near surface porphyry targets within the greater Cajueiro project

- Third Party Validation

- Aura Minerals ($3.5 B): 11%

- Crescat Capital: 16%

- Coming Catalysts

- Assays from the deep hole “Maria Bonita”

- Expanding resource at “Maria Bonita”

- Expanding resource at “Cajueiro Central”

- Scout drilling #5 prioritized porphyry targets

The Case in Short

1.4 Moz, which is extremely likely to grow, coupled with the involvement of an experienced Brazilian gold miner in the form of Aura Minerals provides the Margin of Safet. The “free” optionality is that this might turn into a multimillion ounce gold district and it might not take that long to find out. I consider Altamira to be a Low-to-Medium Risk/High Reward case.

The Case

With 1.7 Moz of global resources within the Cajueiro project I believe that Altamira already has reached a gold endowment of near surface ounces that warrants building a mine. Further evidence of this is Aura Mineral’s second financing participation in a row. Aura is a successful mid tier miner who currently operates three mines in Brazil and are known to be builders/operators and not explorers. This suggests to me that they believe that Cajuiero has a good chance of becoming a mine. All this provides the “Margin of Safety” as I see it.

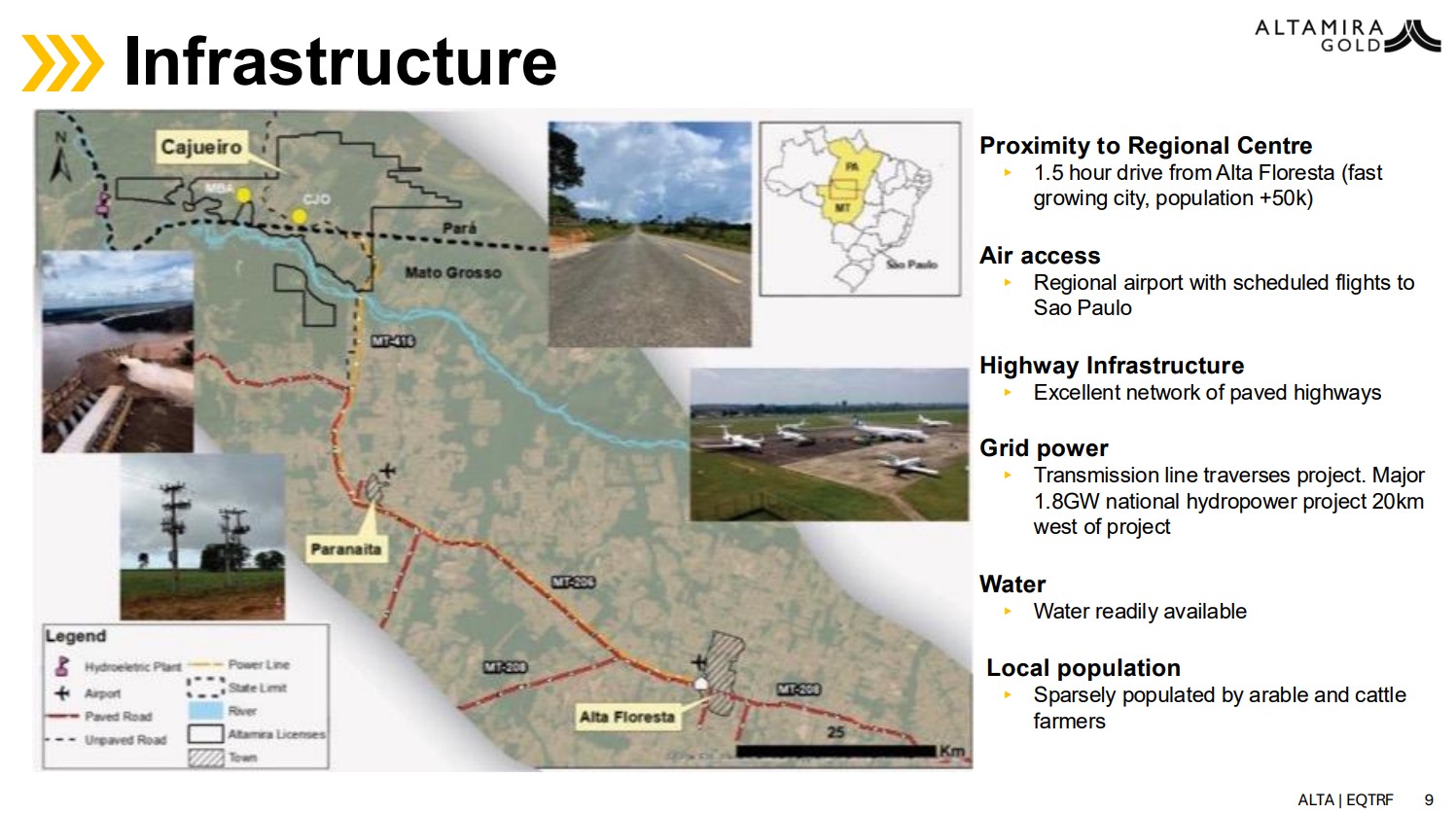

Infrastructure

Description of Cajueiro:

The Cajueiro project is located approximately 75km NW of the town of Alta Floresta in the state of Mato Grosso (Figure 1) in central western Brazil. The project is easily accessible by road, lies on open farmland and has grid power and a local water supply.

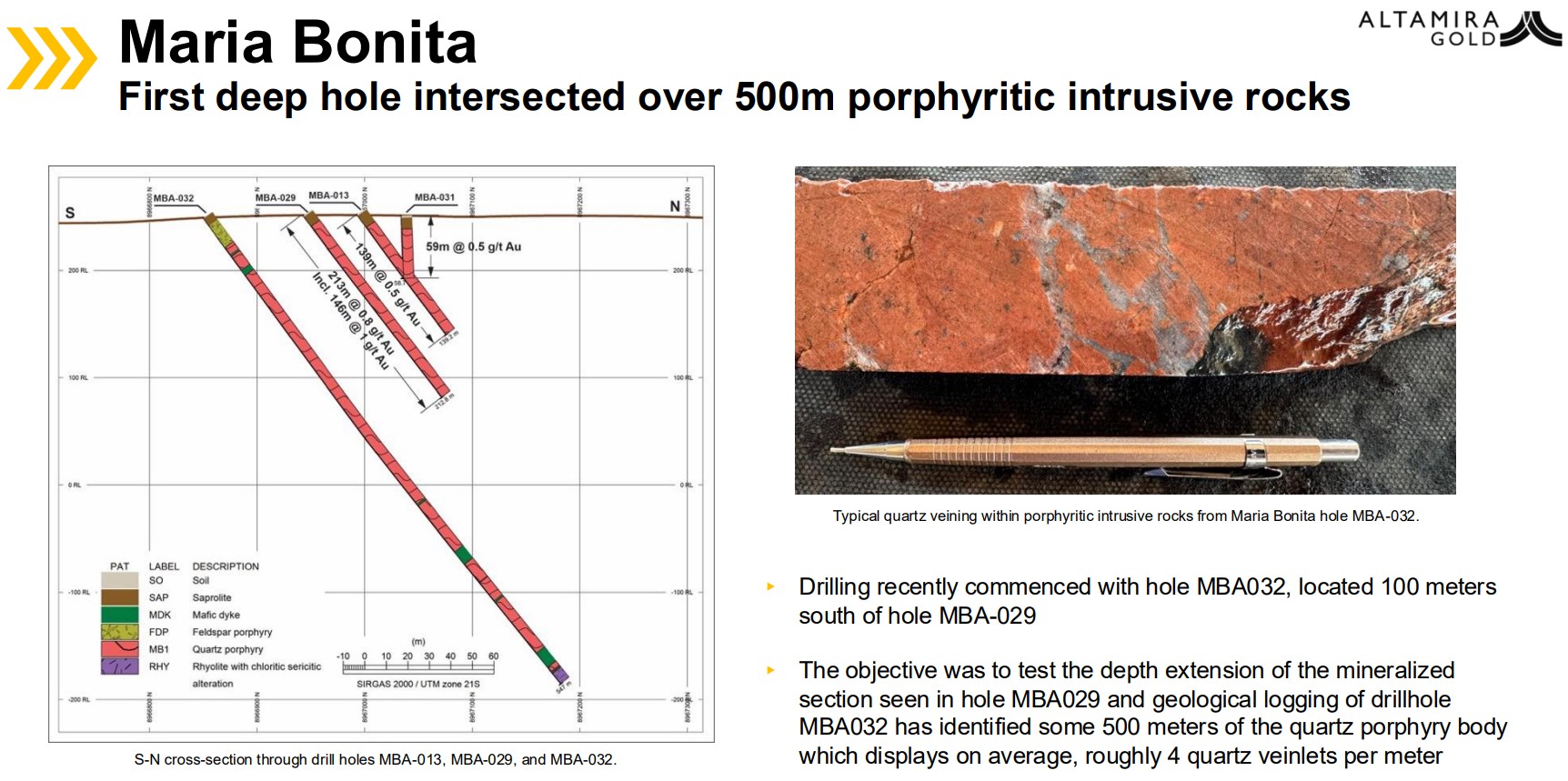

What makes this story much more interesting however is the Margin of Safety combined with the significant exploration potential in the Cajueiro project. This was recently highlighted as Altamira put out news that a deep hole has been drilled at Maria Bonita and it encountered 500 meters of “brecciated and highly altered porphyritic intrusive rocks” starting at 34.3 meters. This hole is collared 100 meters south of a prior hole which assayed 213m @ 0.8g/t gold from surface including 146m @ 1g/t gold (>100 gram*meters):

Comments in the news release:

CEO Mike Bennett commented; “The first deep hole at Maria Bonita intersected over 500m of highly altered porphyritic rocks and suggests that the intrusive system there could be significantly larger than currently envisaged. Additional holes will be completed at Maria Bonita once we have received the results from this first deep hole. In addition, the surface mapping and sample results from the untested Tavares Norte target, located 1.5km east of Maria Bonia are highly encouraging and suggest the possible presence of another porphyry system. Initial drill testing of this target is being planned as part of the current program.”

Here is Quinton Hennigh commenting on the deep hole and new targets:

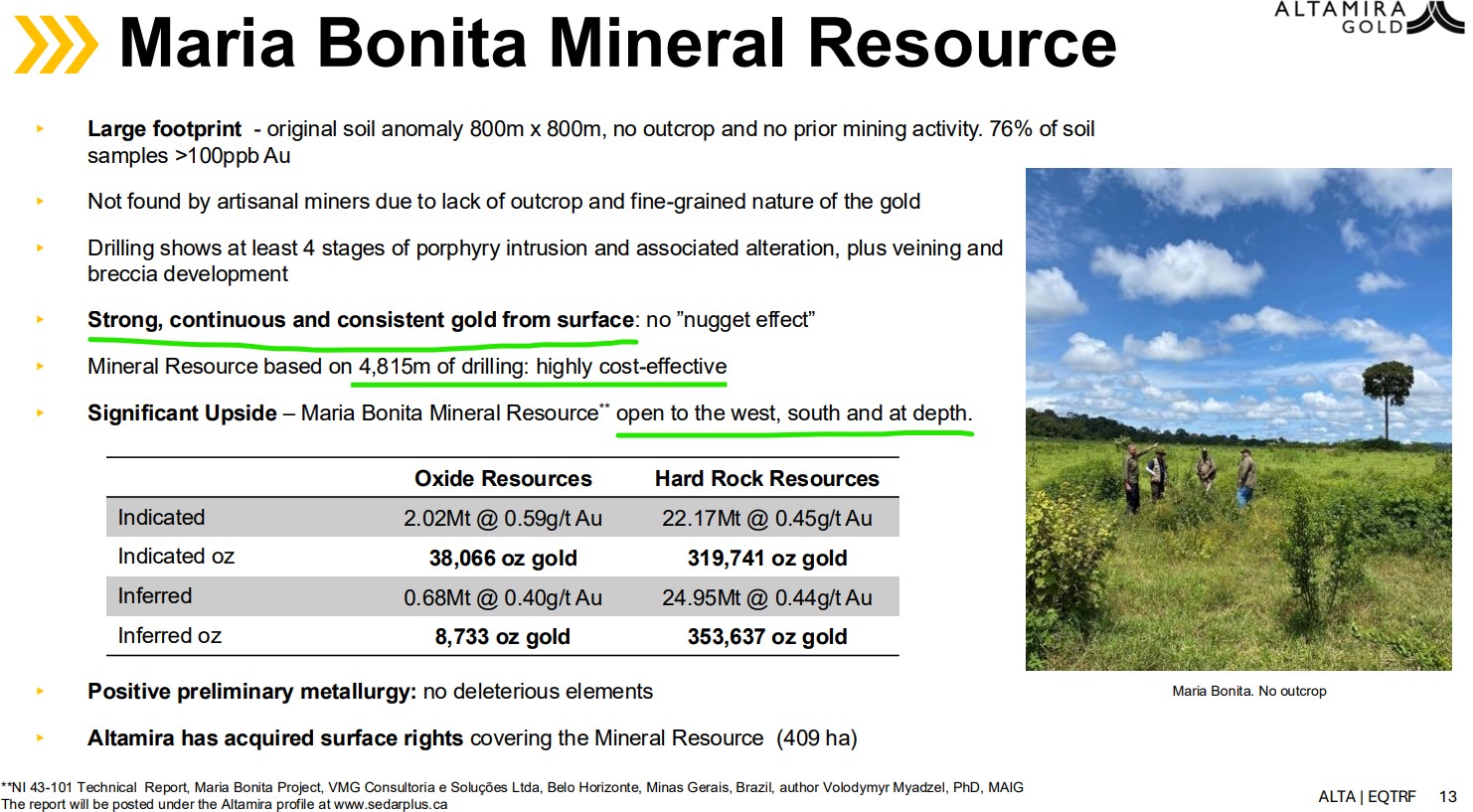

The beauty of a deposit such as Maria Bonita (Porphyry/RIRGS) is that it can rapidly grow just like Valley (Snowline). The current resource of around 700 Koz was produced from a mere 4,816 m of drilling:

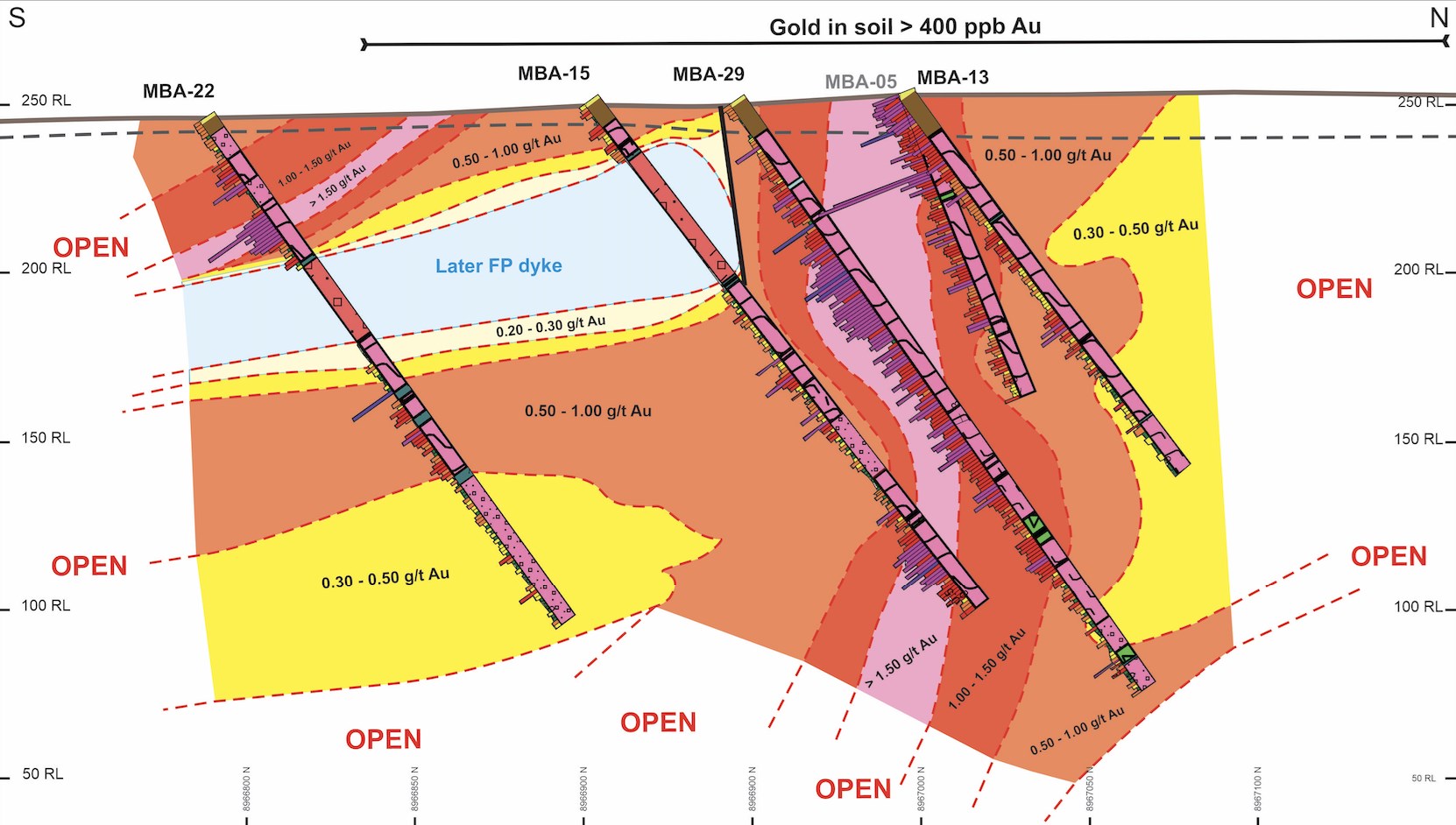

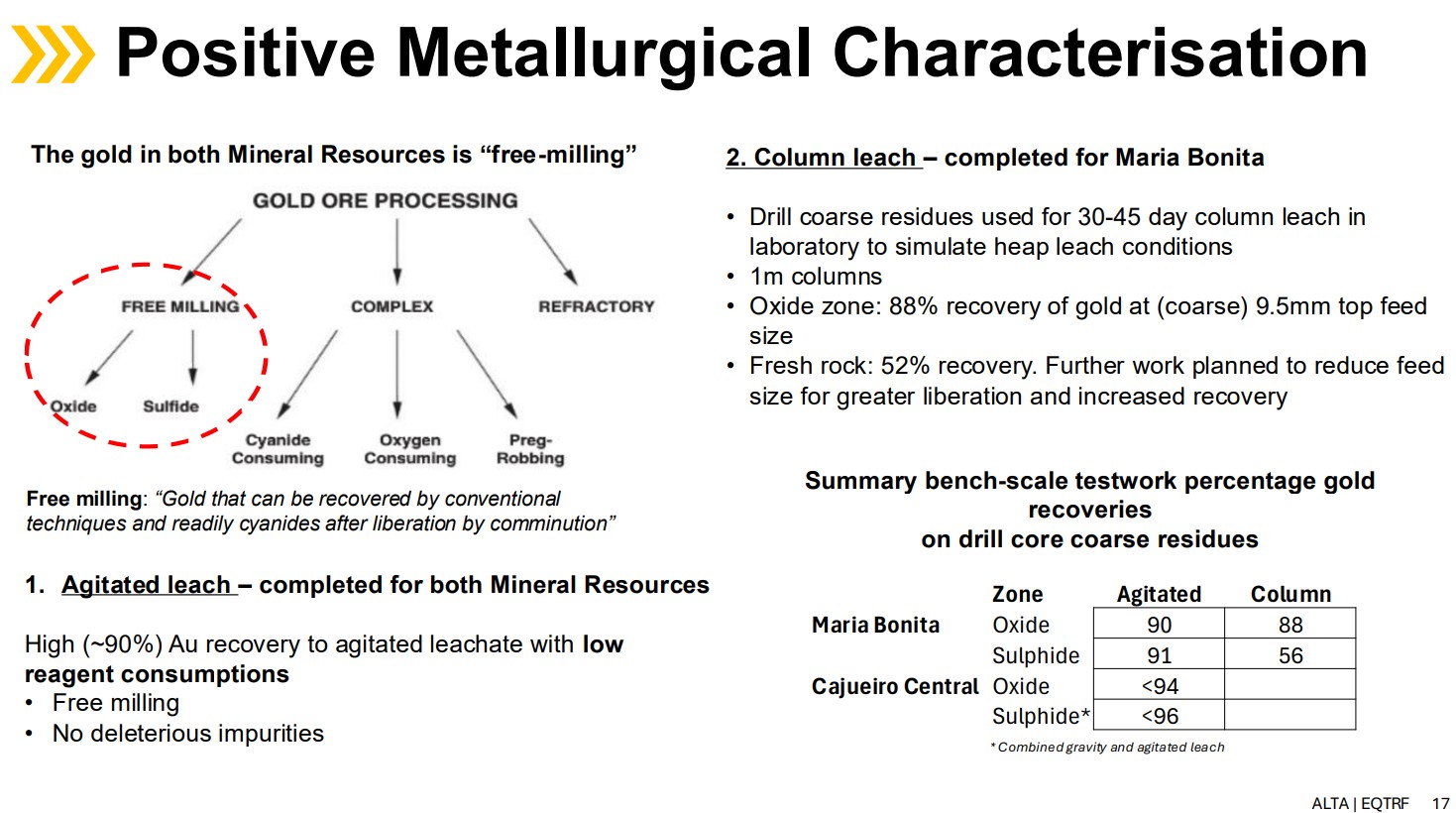

The grades are pretty low but the system starts at surface, the metallurgy appears to be very favorable, and there seems to be disseminated mineralization all over the place:

This recently reported first deep hole, encountering 500 meters of porphyry rock, is more than double the length of the holes in the picture above. Thus it does not take a rocket scientist to figure out that Maria Bonita is likely to grow. And perhaps grow quickly. If the resource was simply to “just” double at Mara Bonita then the global resource at Cajueiro is already at 2.4 Moz. This would already be a sizeable resource and something I very much think will turn into a mine (I think Aura Mineral’s would agree).

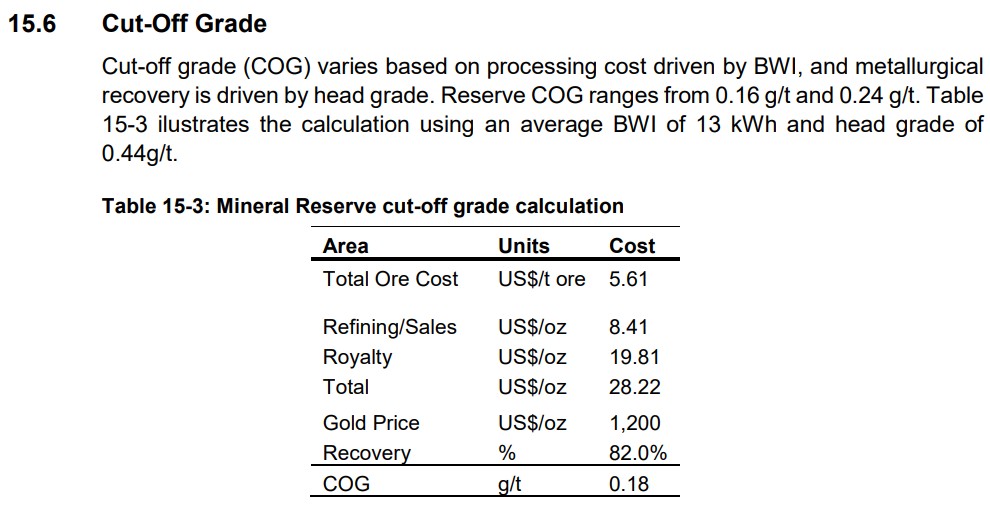

It is also noteworthy that Kinross Gold’s flagship mine called “Paractu” is located in Brazil and is a huge low grade deposit:

The cut-off grades in the latest technical report for Paracatu:

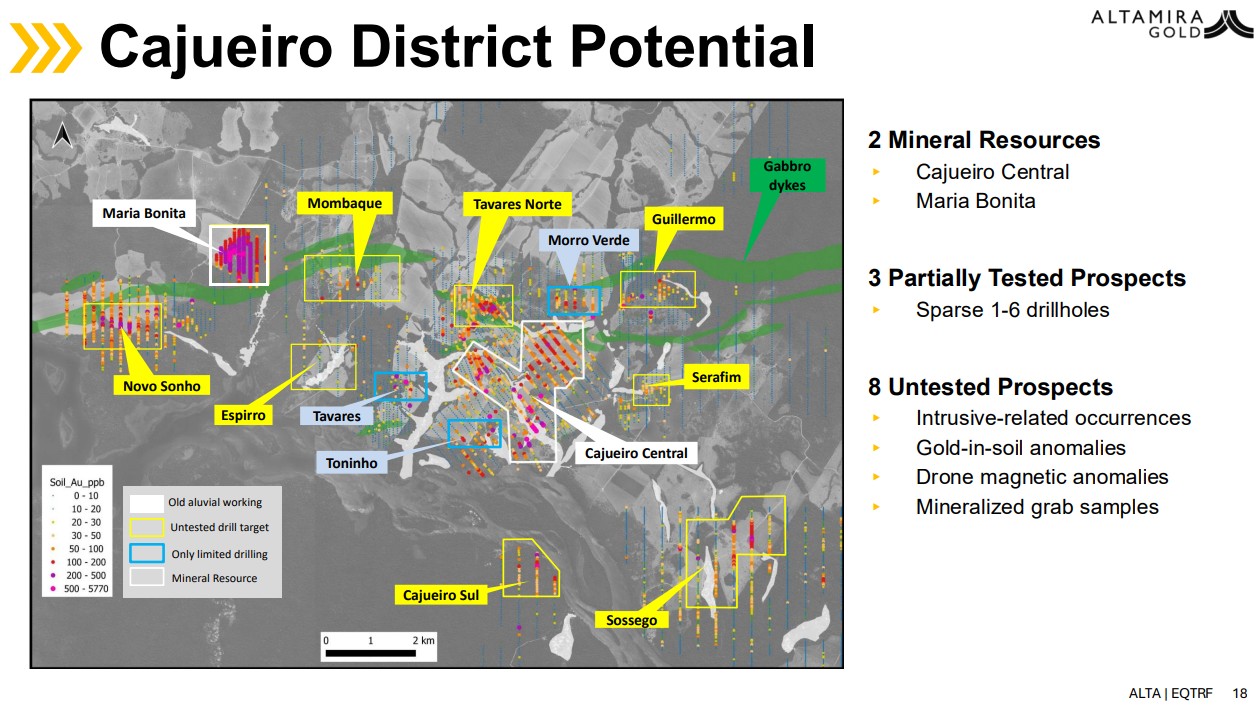

… Of course this is a giant deposit that enjoys economies of scale but the point is that large open pit deposits, with favorable metallurgy, can certainly work in Brazil (Again, I point to the involvement of Aura Minerals for further proof). But it gets better yet as the actual blue sky case is that there might be even more near surface porphyry deposits to discover as per the latest news release:

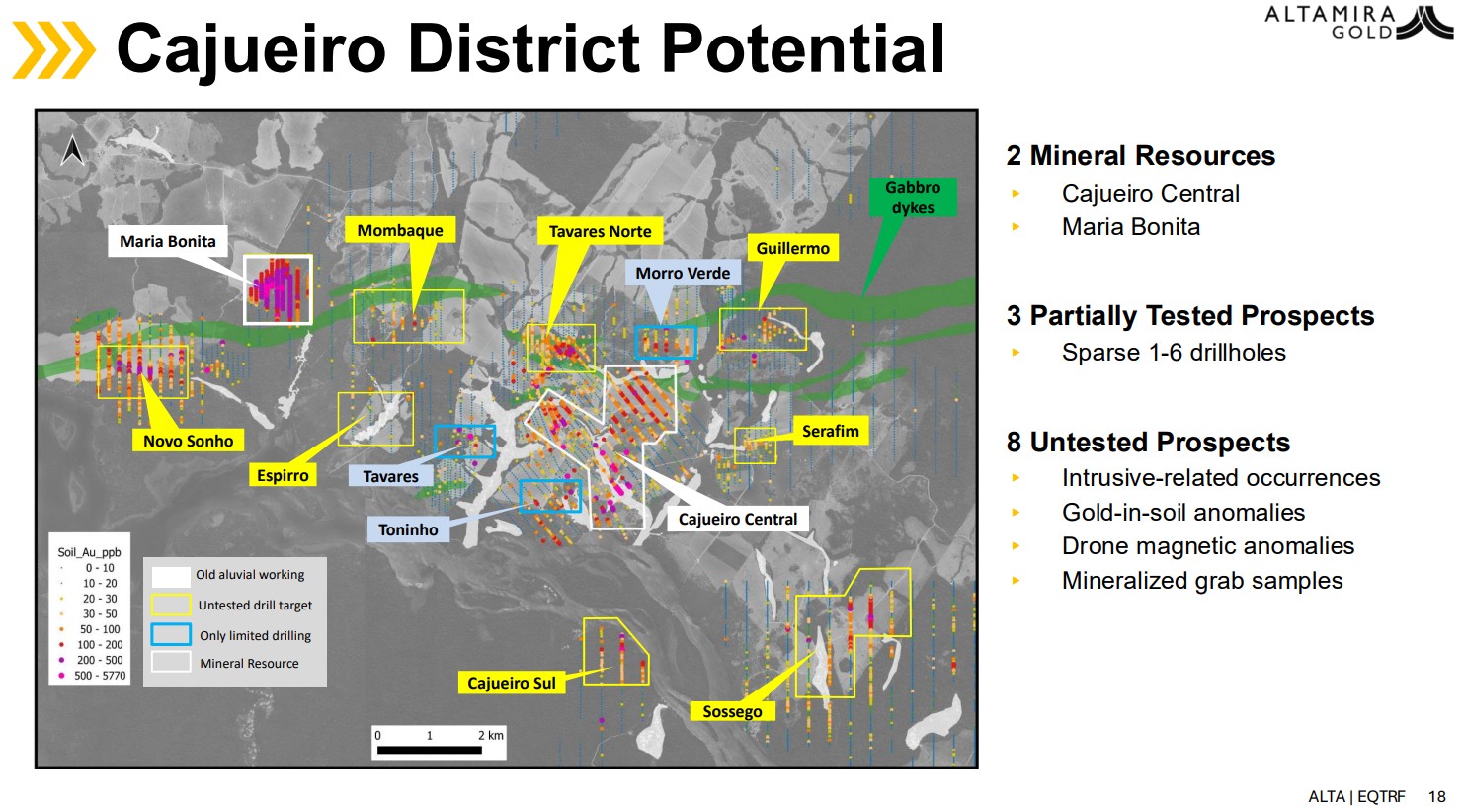

“The Maria Bonita porphyry gold deposit is interpreted as part of a district-scale, porphyry-related mineralizing event. There are currently eight additional porphyry gold targets awaiting scout drill testing over an 8km radius from the Cajueiro Central resource (Figure 2). Three partially tested drill targets lie outside the current Cajueiro Central mineral resource. Drilling is planned for these targets and will commence as soon as a second rig becomes available.”

… Obviously the potential in this picture above is that the so far known deposits, which are open, will grow and additional discoveries are made leading to a future with multiple deposits feeding a central processing facility. And as stated earlier the preliminary work suggests favorable metallurgy for both so far known deposits:

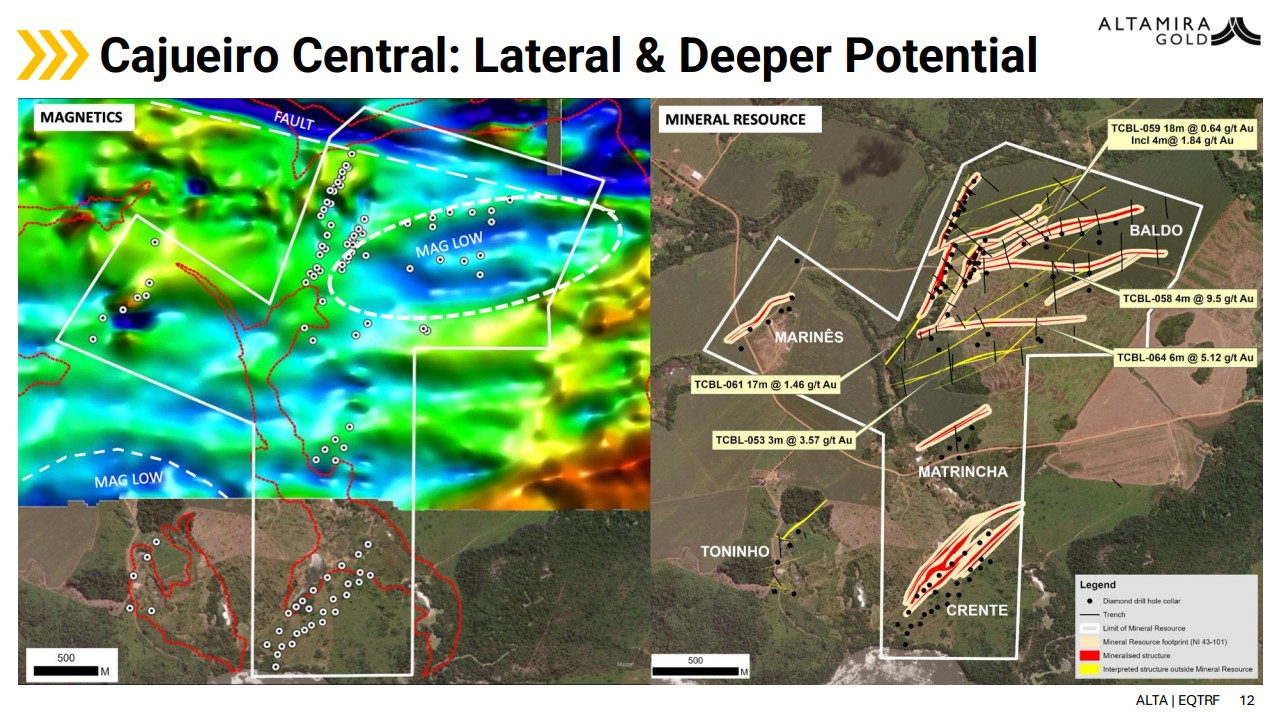

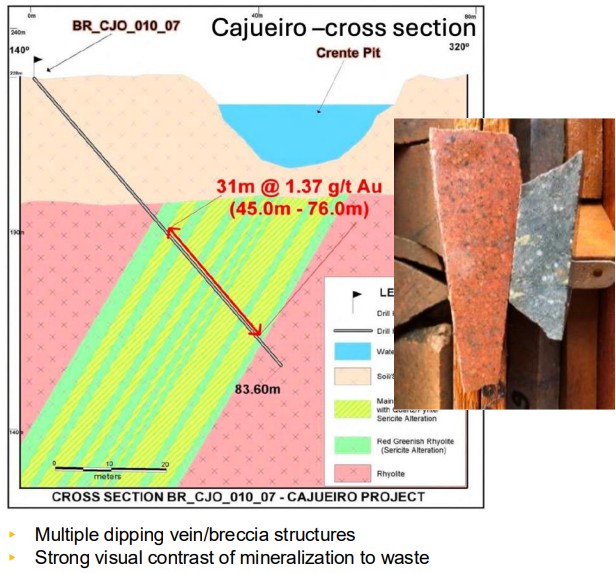

The Cajueiro Central deposit is also open and I would expect it to grow both laterally and at depth with more drilling. Below are interpreted structures outside the Mineral Resource as well as some trenches such as 17 m at 1.46 gpt which is well outside any resource area:

It is also wide open at depth and has only been shallowly drilled so far:

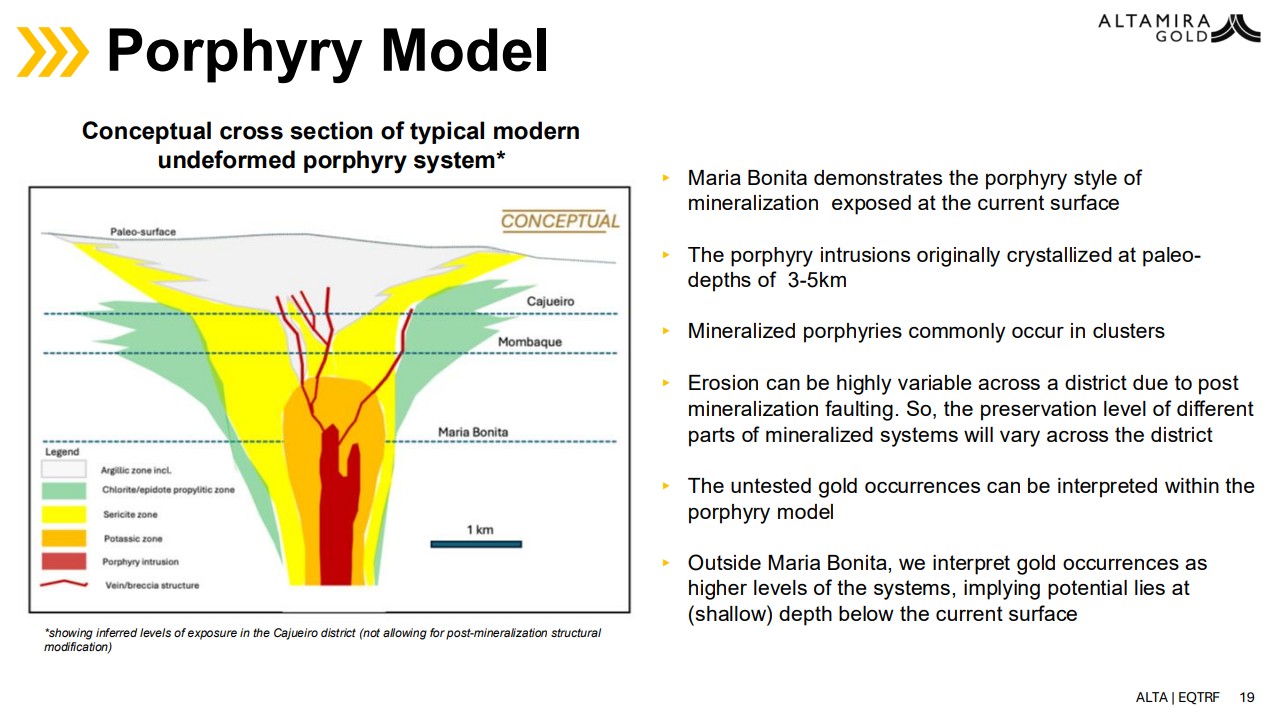

Both Maria Bonita and the Central Cajueiro depost are believed to be different parts of Porphyry systems:

Porpheries tend to show up in clusters so the belief is that all these targets that have been identified withing the greater Cajueiro project are porphyries and/or derivatives of porphyry systems:

… Note the scale bar. These are some very large targets.

Closing Thoughts

I simply believe Altamira provides a rare Low-to-Medium Risk / High Reward case at the current Market Cap. To have a mining company with extensive Brazillian gold mining experience such as Aura Minerals ($3.5 B) signals that there is probably a high chance that there will eventually be a mine at Cajueiro. From that perspective, with 1.4 Moz of gold banked already, I do not think the MCAP of Altamira is high even compared to what is already known. The kicker is that I think they could end up finding 3-5 Moz or more. Just Maria Bonita and Cajueiro Central I believe will get them over 2 Moz (Maybe even Maria Bonita alone). If they end up hitting on any of the #5 targets to be tested then the visible upside potential could increase quite quickly. I also think this is a project that will be able to get into production and if things go well this will be a multimillion ounce district in the next couple of years, maybe with material permits in hand, while gold is $4,000-$5,000… This is of course the blue sky scenario I see which could create a 10+ bagger. Emphasis on COULD. Thankfully, nothing of the sort is priced in today which is why I like the bet.

Amateur TA

If I did not know any better is seems Altamira recently broke out of a 10 year long trend line:

Note: I own shares of Altamira Gold and the company is a passive banner sponsor so consider me highly biased. Always do your own due diligence and form your own opinions. Investing in junior miners can be very risky and never invest money you cannot afford to lose. This is not investing advice. I cannot guarantee the accuracy of the information in this article. I share neither your losses or your gains. Assume I might buy or sell shares at any time. I will not be able to hold anyone’s hands 24/7.

Best regards,

The Hedgeless Horseman