GFG Resources (GFG) Part 2: Notes From Call With Management

(Part 1 in the series covering GFG Resources can be found HERE.)

Below is a summation of the information received from my call with CEO Brian Skanderbeg and VP Marc Lepage of GFG Resources last week, Enjoy!

- The team had the Rattlesnake Hills project on their radar even before their success with Claude Resources was a reality and they became “free agents”.

- John Awde (CEO of Gold Standard Ventures and founder/director of GFG) consolidated the Rattlesnake Hills (RSH) district at the depths of the bear market in 2015.

- Consolidation was possible since there were no competitors during the 2015 since the sector ran around with its hair on fire.

- Awde presented the now “jobless” ex management team of Claude Resources with the opportunity of joining GFG Resources and make Rattlesnake Hills their next project, which they obviously said yes to.

- The ex Claude management team has a long history together.

- Tim Brown (the 21-year Cripple Creek veteran) was already with GFG when the Claude team joined the company and on top of that has a history with Quinton Hennigh and while he was at Anglo he visited the project several times!

- The Wharf mine is a highly profitable operation (which I will cover later in “Part 3”).

- Alkalic systems like RSH, Wharf and Cripple Creek tend to occur in districts and hosts multiple deposits.

- RSH will have seen a total of 95,000 m drilled after the current campaign is finished.

- $40 M has been invested in RSH prior to GFG taking over the project ($40 M of sunk costs bought up for pennies on the dollar).

- All GFG directors have multiple experiences of developing and successfully selling companies (de Jong just recently sold Integra for $590 M to Eldorado Gold for example).

- GFG shareholders include prominent institutional investor such as Sentry, US Global, Machenzie, AGF and Zebra Holdings (who participated in the private placement and has bought shares in the open market).

- CEO Brian Skanderbeg and company found/director John Awde are the largest shareholders, each with a 6%-8% stake in the company.

- Insiders are currently in a “black out period”, which means they cannot buy additional shares at this point in time.

- Treasury stands at approximately US$3.5M. This will be enough to meet their 2017 budget.

- Quinton probably departed from Evolving Gold due to dispute with the new CEO.

- Agnico-Eagle terminated the JV before ongoing exploration was even concluded (I will cover this more later in “Part 3”).

- Brian has spoken with employees from Agnico-Eagle that worked on RSH, who confirmed that they did not terminate the JV because of disappointments regarding the project.

- Management does not see any major obstacles in terms of permitting (no more than the usual obstacles for any potential developer at least).

- Water and electricity should be doable.

- The GFG story has gotten a lot of traction lately with over a 120 “one on one” meetings with potential investors.

- Management’s schedule is packed with upcoming marketing efforts over the next few months. For example:

- Traveling to major cities in both North America as well as Europe.

- One of 10 companies that are invited to RBC Capital Market’s “Rising Stars” even in Toronto.

- Will be attending two shows held in Colorado next month.

- Analyst and investor site visit in September.

- Brian expects there will be an additional one or two analysts covering the company in the not too distant future.

Potential production scenarios depending on exploration success:

Obs! The following is highly theoretical at this point in time!

- Small operation (If there was 1 Moz+ in resource) : Mine oxides (Higher recovery)

- Larger operation (If there was 2 Moz+ in resource): Mine oxides + sulphides (Blended with decreased recovery)

(I will expand more on this as well as metallurgy in “Part 3”.)

Horseman’s personal thoughts:

I found Brian and Marc to be very professional and also seem very keen on keeping a good relationship with the company’s fellow shareholders. Marc has been very generous with his time both before and after the call, answering any questions that I might have had. On that note I actually e-mailed Marc and asked if he could expand on my take that Brian seemed VERY excited about the team potentially having “solved” the structural puzzle at RSH, and this was his response:

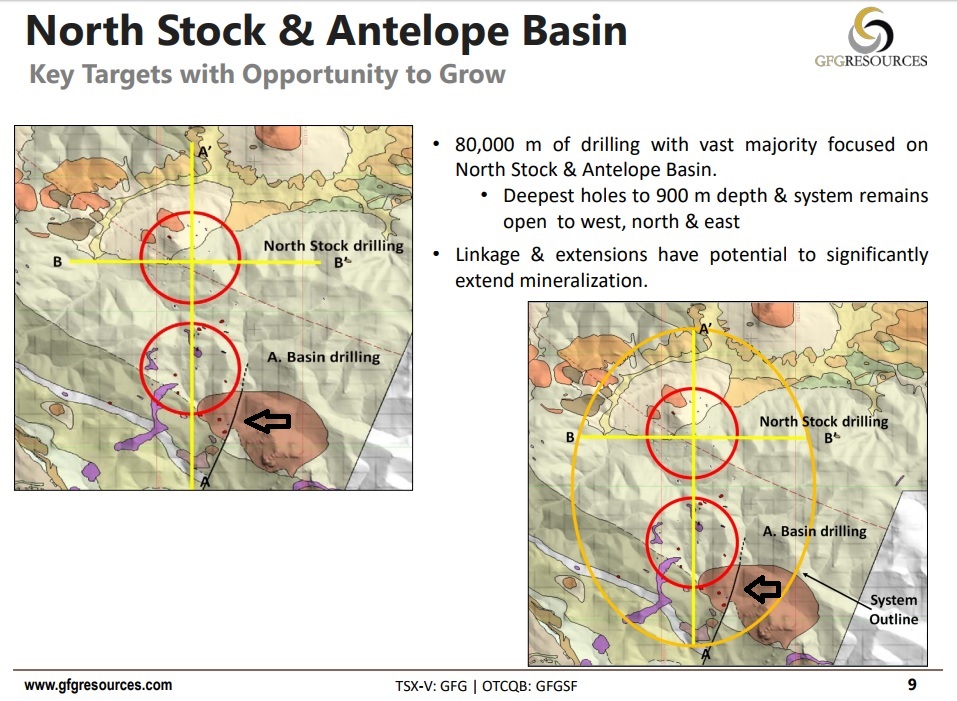

“We have done a lot more data work (5,000+ more soil samples, VTEM survey and structural modeling) that had never been done. A lot of this work was driven by Tim Brown based on his experience at Cripple Creek (specifically the VTEM survey). This analysis was a key tool that worked really well for him at Cripple Creek to find gold mineralization. Also, we have consolidated all the information (see p. 12 of presentation) into one program which has given us a much better understanding of the district and will help identify the controls of the gold mineralization. The black line (potentially a controlling structure) on p.9 of the presentation is derived from an M. Sc thesis completed under EVG. We interpret the structure to have continuity to the north and may be important at the new discovery – the Cowboy target. There are many other important structures that were not historically mapped/interpreted given the depth of oxidation and difficulty in surface mapping in this terrain. This understanding is very important and is why Brian was enthusiastic about the structural interpretation.”

P. 9 from the presentation.

As a final note I would encourage everyone to watch the following presentations with CEO Brian Skanderbeg:

- Video presentation from the “2017 European Gold Forum” held in Zurich, Switzerland.

- Video interview from “Cambridge House”.