Lion One Metals: Boredom = Cheap

- Lion One had to buy new drill rigs in order to drill the deeper parts of Tuvatu = Delays

- Wet season = Delays

- Strict COVID restrictions = Delays

Lion One’s share priced peaked in August of last year and has since then been drifting lower. I think a big reason for this is simply because the story has been “boring” in the last couple of months due to delays. However, there has been some assay results recently which extended the vertical strike, from the existing resource, by around 200m. If one listened to Quinton’s recent interview with Cory Fleck of Kereport one would have heard that the endowment per vertical meter at Tuvatu is around 2,500 ounces give or take. So in other words one can envision that Lion One has potentially added around 500,000 ounces of “inferred” gold with a rather limited drill campaign so far…

Food For Thought:

- The latest Economic Study on the Tuvatu “starter project” showed a NPV of US$243 M and IRR of 85% at a gold price of US$2,000.

- … From 331,386 ounces of recovered gold

- Lion One has around C$63 M in cash

- Lion One current has an Enterprise Value of around US$132 M

Now one might wonder what “just” 500,000 ounces of inferred gold endowment would add in value at the end of the day(?).

Now one might also wonder what Lion One could be worth at the end of the day if the mineralization goes a lot deeper at Tuvatu (Alkaline systems tend to go very deep):

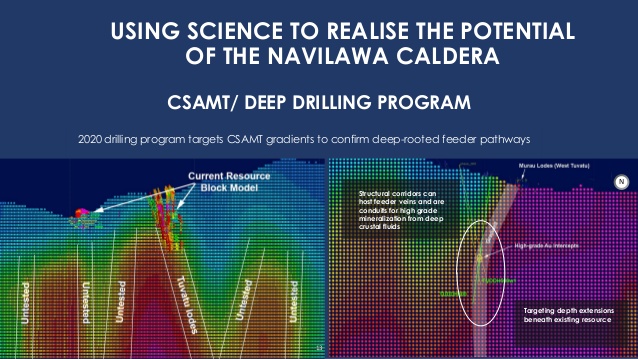

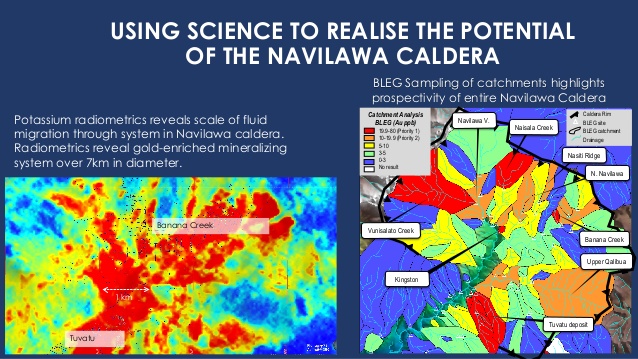

… And one might wonder what Lion One could be worth at the end of the day if one or more of those inferred targets in the slide above have economic mineralization as well. One might also wonder what Lion One could be worth at the end of the day if there are more lodes within the 7km in diameter caldera where there is “golden smoke” everywhere:

Discounts due to investors simply being bored are the best form of discounts because nothing has changed in terms of current value or future potential. One day Lion One is going to be “hot” again and then the market will “re-discover” what has been there all along and suddenly give the company credit for how good the project looks (There is nothing like price to change sentiment). Taking advantage of people selling an undervalued stock because they are bored is a boring way to make an easy living. Don’t get me wrong, I think Lion One has been very boring recently but I have not forgotten that it’s one of few juniors out there with an actual tier 1 gold exploration project. This has been, and still, is a monster system in my book and one day I think it will be in the hands of a major. Personally I the market will be in “Boring Mode” a while longer because I don’t know many permitted tier 1 projects selling for US$132 M and I prefer to have at least one no brainer to put money into at any point in time.

Note: This is not investment advice. I am not a geologist nor am I a mining engineer. This article is speculative and I can not guarantee 100% accuracy. Junior miners can be very volatile and risky. I have bought shares of Lion One Metals is in the open market and have participated in one private placement. I can buy or sell shares at any point in time. I was not paid by any entity to write this article but the company is a passive banner sponsor of The Hedgeless Horseman. Therefore you should assume I am biased so always do your own due diligence and make up your own mind as always.

Best regards,

Erik Wetterling aka “The Hedgeless Horseman”

Follow me on twitter: https://twitter.com/Comm_Invest

Follow me on CEO.ca: https://ceo.ca/@hhorseman

Follow me on Youtube: My channel

Goldbugs already anticipating massive market crash – there’s no other explanation for this relentless selling on no news.

I wonder what a major would pay for Lion1 with gold at 8K and PP reserves of 20 million oz ?

And what would NEM pay for NuLegacy if they find 50 million oz of gold in NV?

Lion ~ LOMLF

TAX LOSS selling will end by about the 29th, I believe. I never get the “exact last date to recognize a capital loss” but with settlement 2 days later, let’s say 12/29 — without looking at a calendar.

I expect LION to reach a resource of at least 5,000,000 ounces. Such an alkaline system is probably larger. With an operating mill and a huge resource that is OPEN to expansion, let’s say worse case is about $300 an ounce. That’s about $1.5 Billion with my forecast. (owning an adday lab is a huge plus as is company owned drills and company trained employee drill teams — at least to a degree.). $1.5Billion / by $200,000,000 shares (assuming extra capital raises) is $7.50 a share.

BUYOUT PROJECTION:. Range. $5 ~ $9, assuming $1850-$1950 gold is my INITIAL ROUGH, ROUGH ESTIMATE. It’s only 83 cents; so even $4 represents a huge gain. Still, I believe that $7-9 is an outside possibility sometime in 2023. Strong Buy

IF gold ever reaches $2,500-$3,000, buyout prices could move accordingly.

Regards, Ed

BORING LOMLF is not only a good thing, it’s a fantastic situation Upside is phenomenal. Lots of patience required.

I intend to wait this out. Remember, the bigger the resource, the higher a potential buyout price. While indicated or probable is the preferred type of resource, I’ll take some widely spaced “inferred” resources.

(Examples: Stepouts of 100 meters continue to indicate high grade gold, assuming indicated & probable reaches a minimum of 3.5 to 4 mil oz. My #’s may be conservative.))

Patient and add shares **especially** if share price weakens. I AM SURPRISED at how little of a following has developed with LOMLF!((?))

I think of NULegacy had 50mm Oz they’d

Have hit more than dust in first 4 holes. Now they could still find 2-3mm Oz which is extremely rare but I think the big elephant find is off the table. Just my opinion

Lion One Metals is pure excitement compared to Irving Resources. Let’s see, ah yes, diversification saved my portfolio once again. Thanks for the write-up on Lion One.

I picked up some more Lion One and Novo during these boring times. Seems like Quinton’s picks are under attack, but that’s fine. We will come out ahead after this malaise is over. Erik, hope you enjoyed the “bubbles” on Friday…