What I Want to HODL

The beauty of companies in the resource sector is that the customers are the world and that there is always a buyer of a company’s product.

The other side of this is that the companies are price takers and that the sector goes from over supply to under supply, around and around, which means price volatility.

With every cycle low, the high cost producers gets killed. They will either dilute, take on more debt, sell their future (projects) or go bankrupt if that doesn’t work. Anyway you slice it, a bear market usually not only results in a crash of valuation for the high cost company, but often it also leads to a company that is worse off in the coming bull due to said dilution and/or shedding of assets etc.

In other words: Thou shall never HODL a high cost producer or “optionality play” that does not have absolutely rock bottom cash outlays (Unless you are sure that the high cost producer will turn into a low cost producer etc)

The low cost producers are able to survive the downturn and even generate Free Cash Flow when their competitors are fighting for their lives. Not only might they not have to dilute their share structure or sell their future, but they might even be able to brighten their future by picking up additional assets at fire sale prices. Some assets might be 90% compared to the price tag just a few years earlier. This can have insane compounding affects in the long run obviously. Everyone knows the mantra of “buy low, sell high” but how many mining companies have the means to do that when literally everything is selling for a low price? Not many. And even if they have the means, you still need a management team and board that has the fortitude and will to actually go out and do it…

Growth aka “Market Potential”

… Then we have the “issue” of miners eating up their future. A company’s low cost mine(s) won’t be around forever and the “market size” for a given resource company is determined by how many profitable ounces that could be put into production that also adds value. A company can grow through value creating acquisitions (like buying assets during a bear market) and/or it can discover new ounces. The main point is that a miner is never stating and constantly needs to replenish it’s “inventory”. Kirkland Lake for example is able to acquire assets and invest in junior mining companies because they have two of the best mines in the world but both Macassa and Fosterville will run out of ore some day. Kirkland Lake is destined to either make more discoveries or acquire assets in order to not go backwards.

A theoretical company with one project that’s only 100Ha can only grow so much since all it’s potential is limited by what’s in the ground in that 100Ha patch of land. What I like to focus on is finding companies with huge potential in terms of internal growth. With a big project or pipeline of projects (a big “market”) and a currently low “market penetration” (lots more to explore) because then there should be ample room for growth before the company finally “saturates it’s market” and is forced to acquire additional projects in order to grow further.

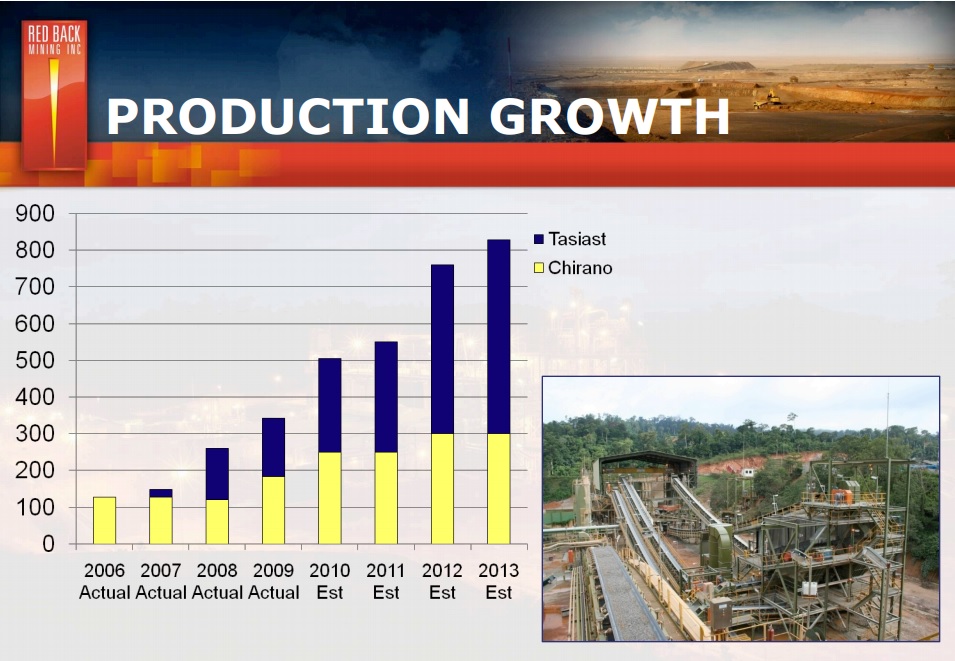

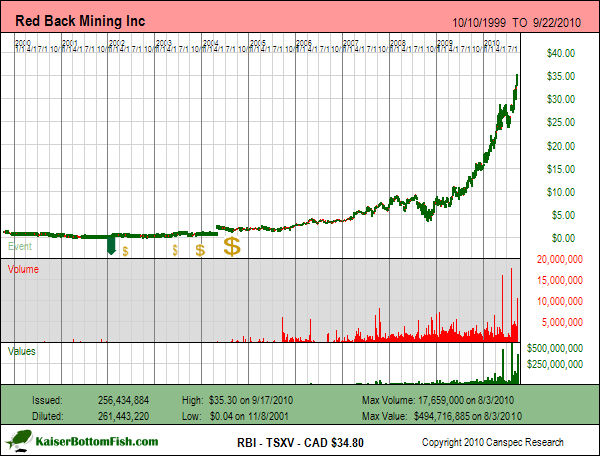

If you own a company that reaches full “market penetration”, in other words have exhausted all internal growth prospects at or near the peak of a resource bull market then there is no option left than buying possibly over-priced assets in order to grow further. If not, then the company will simply start to eat up it’s own future (and thus value) with each passing year and thus shrink instead of grow. How many mature companies that went out to buy assets in order to grow made good acquisitions? Not many. In fact they proceeded to destroy an obscene amount of value when the bear market finally came since they mostly bought marginal assets at inflated prices. Again, why would I want to own a company that is close to maturing that would need to buy it’s growth in a raging bull market? I want to own the companies that are growing and have a lot of potential growth yet to come. The Cindarella story of the last bull market was probably Red Back Mining. Red Back was a Lundin backed gold company that made discoveries and were even able to do a good acquisition that they then proceeded to grow. In the span of a a few years it grew and grew and went from being a junior explorer to being a mid tier producer and finally being bought for around C$11B by Kinross Gold (who was the major company that wanted/needed to grow through acquisitions during the peak of the gold bull).

Here is the production growth chart for Red Back Mining as well as it’s stock chart:

Red Back Mining

(One could obviously argue that it is redundant and probably foolish to try and trade a stock with a strong tailwind of fundamental growth)

… THE Dream ought to be to find a juniors that can just grow and grow over multiple years and just keep getting more and more valuable because then it doesn’t really matter if the gold mania is 2 or 5 years off because whenever it comes the said company ought to be the most valuable it’s ever been anyway. In other words the time would be on it’s side and the intrinsic value would keep going higher and be higher with each passing year. If it gets bought out in five years, that’s five years that saw the company creating value.

A mature junior and/or a junior with limited funds and/or prospects is a junior that doesn’t have time on it’s side. Instead of simply becoming more valuable as the years pass by, it just sit’s there and stays approximately the same. In other words, if gold hit’s $2,000 tomorrow or $2,000 a year from now, the value and potential take out price would be exactly the same, all else equal. In contrast, the growing company would have seen one additional year for value creation and thus be worth even more when gold hit $2,000 a year from now. As you probably understand I do not like the former scenario above and that’s why I want to focus on finding companies with the potential for a LOT of run way for internal, high-quality growth. Thus I am not particularly keen on “mature” junior companies that have one advanced project and not much else. Let’s say a junior developer is able to actually put their project into production but it has no real pipeline for growth. How will it proceed to create value when it has already started eating it’s own future?

Take Pure Gold for example which a lot of people seem to like. It’s one of the better juniors around, but what if the gold bull takes off tomorrow and the whole sector revalues? Sure, it should revalue as well, but lets say they get into production in a few years and everyone is happy. What’s the next steps? If they start making good cash, others will have started making good cash as well and if it’s not taken over then it will need to grow at some point since again, the company is continuously eating up it’s own future and thus shrinking. If it goes for external growth then it might need to pay up, and that’s no guarantee of being value adding (although the management team is a good one). It could of course look for internal growth aka drilling for new discoveries. That’s probably the best option since nothing suggests that they have drilled the limits of the system. Are they going to find the equivalent value of another mine anytime soon though? That’s unlikely but not impossible of course. Then what? How many mines could their land package be hiding? I have no idea, but I doubt there is potential for them to double and then double production every n:th year. With all that said, Pure Gold is a solid and very de-risked play, but it’s simply not my cup of tea (for better or for worse).

I want to be able to have answers for consecutive “THEN WHAT?”…

both because I want to avoid the need for external growth as well as the fact that the market also constantly asks this question and you get a “carrot premium”

So what are some examples of companies that look pretty suited for a world with higher asset prices across the board…?

I could come up with a few names. In the junior producer space we have companies such as Premier Gold, Calibre Mining and Argonaut Gold. All companies are of course eating up their future at the moment, but they also have a pretty solid pipeline of projects that could allow them (if successful) to grow for many years without needing to look for potentially over-priced growth that could lead to disaster when the bear comes around. Minera Alamos looks to have a pretty good pipeline of low CAPEX projects that could sustain their growth for quite some time as well as exploration potential for further internal growth. Furthermore, the projects require so little capital that the company is already well underway of building their first project and the coming cash flow could really speed up the growth. In other words, these guys could start small and proceed to compound it’s value by more aggressive exploration and/or start working on their next project. This is different than say Pure Gold who needs much more capital, has a longer build time and “only” has exploration as a way of _potentially_ growing. This further high-lights the importance of cash flow as an obvious way to speed up growth. Either a junior (explorer) needs good access of capital, which usually only happens if they are onto something very promising, or it needs to be a producer or at least have means of quickly becoming a producer in order to grow faster than the average junior.

In short: The companies mentioned above a) have something, b) have pretty reliable ways to grow and c) The growth prospects are probably enough to last for many years which is the basis for my current strategy…

I personally look for juniors that already have SOMETHING or probably have SOMETHING with the potential to have a LOT

… It sounds simple enough but in my opinion there are not a lot of juniors that fit that bill. I would urge you to also ponder these next few questions:

Would you want to own a grass root explorer with ONE asset that may or may not even have any gold or silver that would give the stock some beta if the metals starts rocking?

What’s the beta on zero ounces?

In other words:

I am not keen on looking for growth ONLY. I want a junior that has something banked or probably has something banked AND a lot of growth potential. In that case you got some beta and you might end up with a company that has a lot in a few years when gold might be closer to $3,000 or whatever. Furthermore I would like to own something that could start off small but has the potential to become an “empire” of assets. Preferably this would be done through finding large, high-quality deposits because there is no shortage of mediocre deposits out there today. Barring that I would want to see high-margin projects that could actually get build even though they might not be considered company makers on their own right. At least it would be growth in free cash flow.

Even though I think Premier Gold, Argonaut Gold and Minera Alamos are juniors that I think fit the bill, there are some who I consider to have even more long term growth potential. Namely… Drum roll please… Novo Resources, Irving Resources and Lion One (Surprise!).

Novo is the king, hands down. If they “crack” any of the semi-craton wide systems then they could have the potential for decades+ of growth within each respective system. If the Egina gravels work (both the high-grade swales and low-grade halo) and are as extensive as Novo believes, then they could have a gold field that covers hundreds or thousands of square kilometers. If that’s the case, then you might have a gold growth stock of a generation. Then there are thousands of square kilometers of ground prospective for Mt Roe conglomerates (Karratha, Contact Creek etc) as well as Hardey Formation conglomerates (Beaton’s Creek, Virgin Creek). Then there’s also the potential for lode gold such as Blue Spec and Talga Talga. These are just the prospects we know of and we should soon find out if they have indeed found something more over the last seven months of grassroot exploration efforts. In other words there is no gold junior on earth that comes close to the growth potential of Novo if they are successful.

Next up would be Irving Resources in my opinion. Not only does Irving have 3+ major targets within the greater Omu Project, where each target could be a major mine in itself, but they also have five or six additional project areas in Japan. The Omu project alone probably hosts more potential than 99% of all juniors entire portfolio and there are obviously a bunch of projects to chomp on when they are done with Omu. The company is also backed by Newmont Goldcorp and they have a mining permit at Omui so they have a) good access to cash and b) could probably see some free cash flow sooner rather than later which is a huge boon.

Two runner ups after that would be Lion One Metals and TriStar Gold. These two are more “de-risked” than both Novo and Irving, at least on paper, since they both have PEAs for their projects already. Not only that, but each have a project with outstanding blue sky potential. Lion One has a potentially huge tier 1 Alkaline Gold system that could host 10Moz+. TriStar Gold has a very large paleoplacer project and the company has only drilled the edges so far and is already up to around 2Moz of total resources. TriStar Gold is very undervalued already on paper and Lion One has a mining lease going for it. Both of these are obviously very de-risked and even though they are one project juniors, their projects are large enough that they could be growing for many years to come and have realistic shot of owning world class assets. Lastly I would say that I think Lion One edges it out by having a mining permit even though TriStar is more undervalued on paper, but it’s probably a pretty close call.

Another company that I consider to have SOMETHING and possibly A LOT would be Cartier Resources, which has a resource on their flagship project and a bunch of good looking projects in the pipeline. I would also add GFG Resources into the discussions since they seem to be on to something over at their very large Timmins properties and we might soon know if they got a piece of something potentially substantial over in Wyoming. Both of these companies could have a lot of years of growth ahead if things come together.

There are obviously a bunch of juniors that have something and might even have something good but few also have good access to capital and a large pipeline of projects to boot.

With every new article that covers my thoughts on investing I hope it has started to become obvious that I didn’t pick my core gold holdings at random but rather that a lot of thought has gone into filtering it down to these three main “pillars”. With that said I am constantly on the lookout for new cases and there are certainly no guarantees that my overall strategy is going to outperform in the coming years. It simply makes sense to me and that’s all one can do which is to invest in a way that suits ones goals, appetite for risk and personality.

Conclusions

What I primarily look for in a junior ATM:

- Juniors that have SOMETHING or probably have something

- Juniors that have an extremely large project or a very large pipeline of projects that could allow them to grow for many years without needing to buy something new in order to keep growing

- Juniors that have a shot of a tier 1-2 deposit(s)

- Juniors that could get into some kind of production themselves in order to get means of growing further

- Juniors that have good enough backing that they have means of growing and adding value without the help of a rising gold price

- This is why I don’t look or care about the price of gold that much nowadays

- If a project is good enough, it should attract capital even if capital is pretty scarce

What I am not that keen on owning ATM:

- Pure grass-root exploration juniors that have little to nothing banked and low odds of finding something

- I don’t want to find myself owning a bunch of juniors with no gold or silver if this bull market starts picking up speed

- Little to no pipeline of projects

- Mature, single asset companies that are not easily funded nor very high margin

- Hard to double the value if gold goes nowhere

- Hard to get to meaningful cash flow that could give them a shot to expand the project pipeline before the bull picks up

One could say that the goal is to be RIGHT ONCE. In other words I want to buy a junior that fit the HODL criteria that I could theoretically just check up on once every X year to see that it’s still growing with more to come.

Note that my strategy is obviously not the “safest” one. If you want to participate in a gold bull but want very little risk of permanent loss of capital then cheap project generators, royalty and streaming companies would probably be the best option. My strategy is much more a combination of a shot at some over-sized returns coupled with relatively low risk for total loss of capital (at least in my opinion). Also keep in mind that this whole article is about what I want to see in a junior that I would plan to HODL through the ups and downs. I have other positions as well that I have no problem letting go off completely if they reach a certain valuation.

(Note: These are not buy or sell recommendations. This is not investment advice. I am not a geologist nor a mining engineer. Always do your own due diligence. I own shares of Novo Resources, Lion One Metals, TriStar Gold and Irving Resources which I have bought in the open market and am thus biased. Novo Resources, TriStar Gold and Lion One Metals are passive banner sponsor on my site. I don’t get paid by anyone or any entity to write these articles.)

Best regards,

The Hedgeless Horseman

Follow me on twitter: https://twitter.com/Comm_Invest

Follow me on CEO.ca: https://ceo.ca/@hhorseman

Follow me on Youtube: My Channel